By Stephen Wu, Economist at CBA:

Key Points:

- We forecast headline CPI rose by 0.9% in Q3 23 (5.1%/yr).

- Trimmed mean CPI is expected to have increased by 1.0%/qtr(4.9%/yr).

- We view the risks to our inflation forecast as skewed to the upside. An outcome in line with our forecast is consistent with monetary policy on hold in November.

Overview:

Headline inflation has eased substantially since reaching a peak of 7.8%/yr in December quarter 2022.

We expect the Q3 23 CPI release (due 25/10) to continue to show that the annual pace of inflation is decelerating. We expect headline consumer prices rose by 0.9%/qtr in Q3 23.

Over 2022, the quarterly pace of inflation tracked between 1.8-2.1%, so this represents a substantial easing. Such an outcome would see the annual headline rate dip further, to 5.1%.

The pulse of underlying inflation, as measured by the trimmed mean CPI, is forecast to have edged a little higher to 1.0%/qtr, from 0.9%/qtr previously.

But base effects from a year ago mean that the annual rate on our forecasts will decline to 4.9%.

For a point of comparison, the RBA’s implied Q3 23 forecasts from their August Statement on Monetary Policy have headline inflation at 1.0%/qtr (5.2%/yr) and trimmed mean CPI inflation at 0.9%/qtr (4.8%/yr).

We note that these forecasts precede the substantial run-up in oil prices that occurred over August and September.

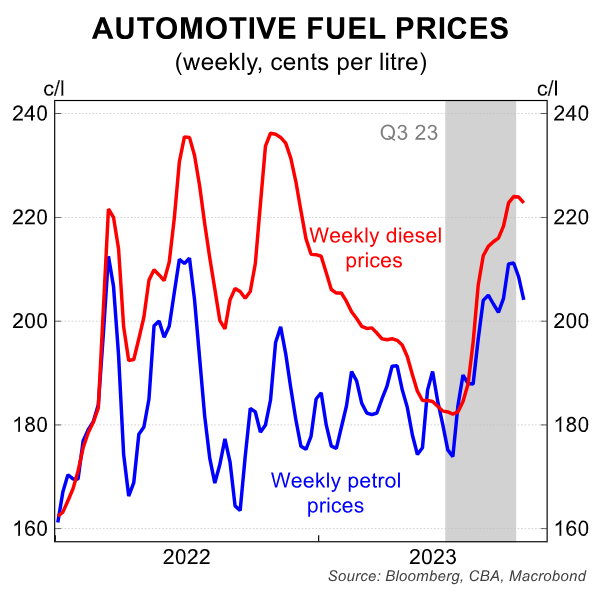

Higher oil prices (up by around 11% over the last two months of the September quarter) mechanically adds to the CPI figure via the impact on automotive fuel, which accounts for about 3½% of the CPI basket, and indirectly through increased freight and other costs for businesses.

As our Head of Australian Economics, Gareth Aird, noted in his report previewing the November RBA Board meeting, our forecast for Q3 23 CPI is broadly similar to the RBA’s implied profile from August.

We believe this is consistent with monetary policy on hold in November.

The ABS’ new monthly CPI indicator provides partial inflation data for the first two months of the quarter. Based on the monthly CPI indicator and uncertainties around particular services components in September, we assess that the risks to our inflation forecast skew to the upside.

The RBA is willing to engineer a slower return to their inflation target in order to preserve the gains made in the labour market.

But as the October Board Minutes stated, “the Board has a low tolerance for a slower return of inflation to target than currently expected” (note that this line was not in the September Board Minutes).

Given the upside risks to our Q3 23 inflation forecast, we are of the view that the November RBA Board meeting is ‘live’ and ascribe a 40% chance of a 25bp rate hike.

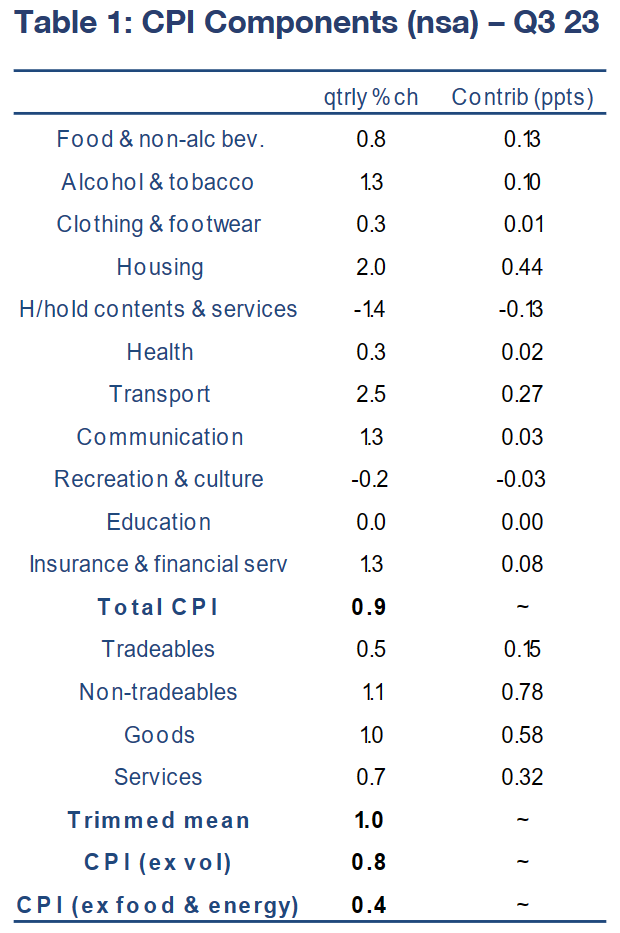

The detail of our Q3 23 CPI call

See table 1 below for our detailed forecasts for the Q3 23 CPI. The main features of our call are as follows:

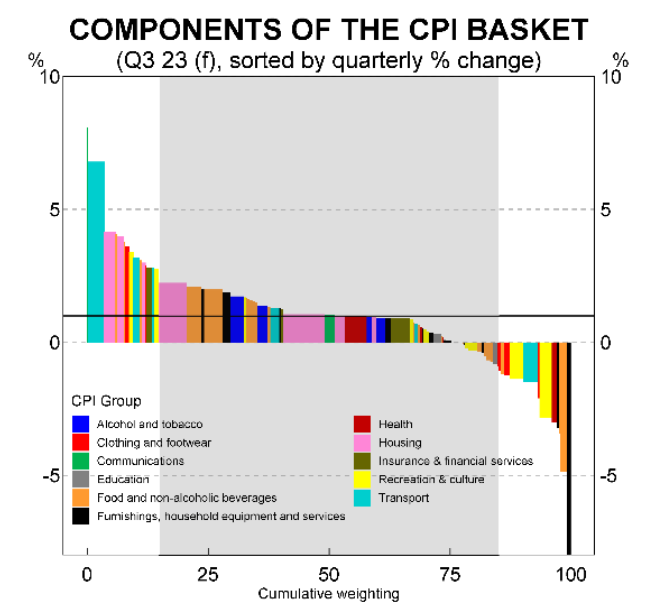

The housing component of the CPI is expected to have seen price rises of 2.0%/qtr, an acceleration from Q2 23.

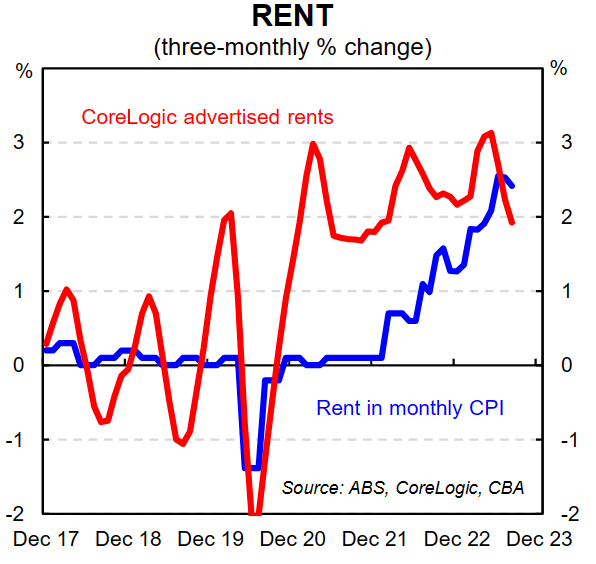

Quarterly rent inflation will have remained elevated, at 2.2%/qtr and well above the pre-pandemic pace of rental inflation.

However, the CPI indicator shows the monthly run rate has eased from 0.8-0.9%/mth in Q2 23 to 0.7%/mth in July and August.

Rental vacancy rates remain at very low levels, but rising average household size in the capital cities are partially offsetting the strength in rental demand from population growth.

Worsening renter affordability and a loosening in the labour market could limit how rent inflation evolves from here.

Quarterly inflation of rents in the CPI has caught up to the pace of advertised rents growth on newly available rental properties in recent months, which has tracked between 2-3%/qtr since 2021.

Transport costs are expected to have risen by 2.5%/qtr, driven by a likely 6.8%/qtr increase in automotive fuel.

Food and non-alcoholic beverages inflation likely moderated to 0.8%/qtr.

Alcohol and tobacco prices are expected to have risen by 1.3%/qtr, as prices are supported by increases in the alcohol and tobacco excise tax.

The tax on tobacco increased by 5% on 1 September 2023, with annual 5% increases budgeted for the next three years.

Insurance & financial services prices likely rose by 1.3%/qtr. The largest driver was insurance (home & home contents and motor vehicle), up by 2.8%/qtr(14.8%/yr).

We anticipate other financial services inflation moderated from its Q2 23 pace.

Clothing & footwear prices likely rose by 0.3%/qtr. The monthly CPI indicator suggests that clothing & footwear prices were up around 0.6%/qtr to August, but we anticipate softening retail demand saw discounting activity, leading to some clothing prices declining in September.

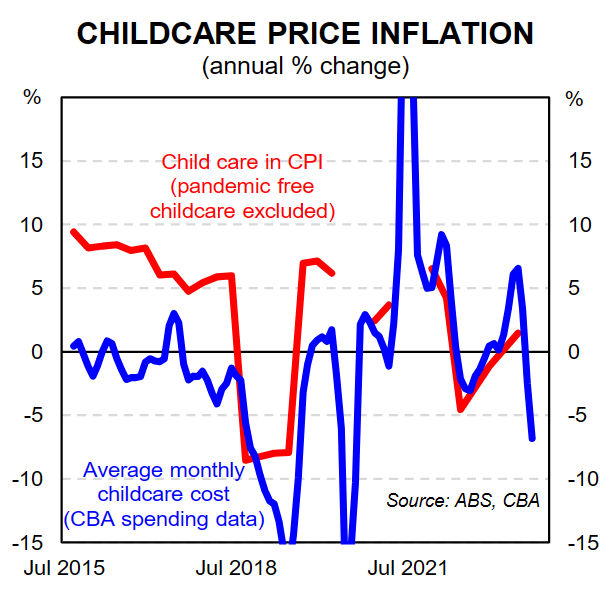

Household contents and services prices are expected to have declined by 1.4%/qtr, detracting from inflation. The key driver is an anticipated 20% fall in childcare prices, subtracting just under 0.2 percentage points from quarterly inflation.

Recreation prices are expected to have declined by 0.4%/qtr, driven by a 2.1%/qtr decline in domestic and international travel & accommodation prices.

On our forecasts, we expect the annual pace of goods inflation moderated further.

We anticipate goods inflation was 4.4%/yr in Q3 23, down from 5.8%/yr in Q2 23. We expect inflation for consumer durables goods to ease further.

In addition, we expect to finally see progress on services disinflation, with our forecast for a step down in annual services inflation to 5.7%/yr, from 6.3% previously, and the first decline in the annual rate in six quarters.

In terms of the other analytical CPI series, we also expect both the annual rate of tradables and non-tradables inflation to moderate.

However, we anticipate the quarterly rate of non-tradables inflation stepped up a little in Q3 23. We expect a slightly stronger underlying trimmed mean CPI inflation rate of 1.0%/qtr relative to the headline rateof 0.9%/qtr (note that the trimmed mean CPI is a seasonally adjusted measure whereas the headline CPI is not).

The large expected decline in childcare prices will weigh on the headline rate, but this will be excluded (trimmed out) from the underlying trimmed mean measure.

Other CPI items expected to be trimmed out from the bottom of the distribution include holiday travel, pharmaceutical products, lamb & goat and vegetables.

On the other end, we expect the large price rises for postal services, automotive fuel, utilities and property rates to be trimmed out.

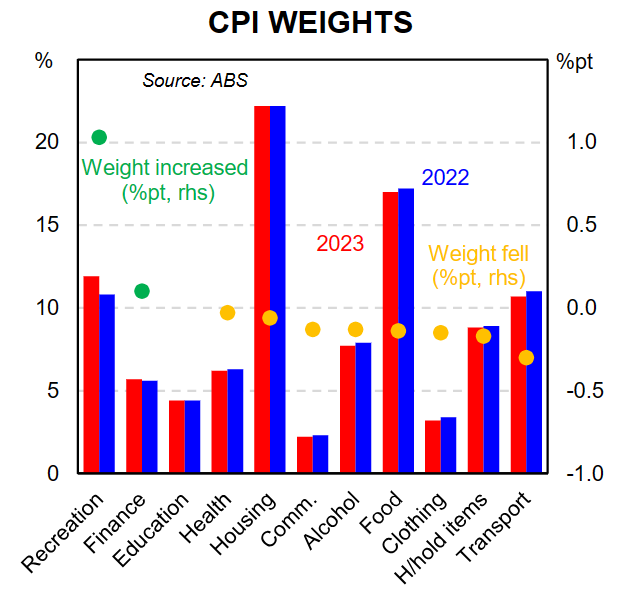

The September quarter CPI release will also see updated weights implemented. Usually this occurs in October (i.e. in the December quarter).

But the ABS has brought this forward this year to account for the increase in international travel & accommodation in the post-pandemic environment.

This component now accounts for 2.84% of the CPI basket, up from 1.85%.

A full re-weight will be conducted in January 2024, and the annual re-weighting will occur in January in future years.