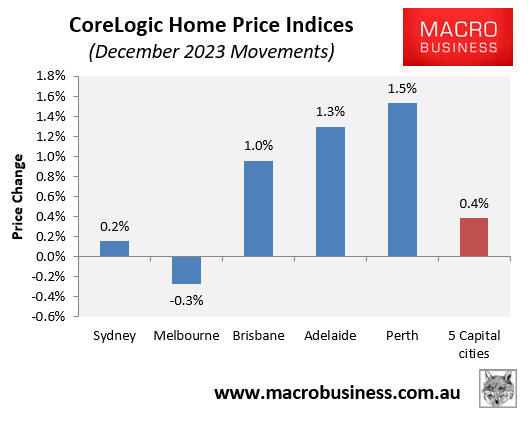

CoreLogic’s daily dwelling values index, which tracks home values across the five major capital city markets, rose by 0.4% in December:

As shown above, the 0.4% gain at the 5-city aggregate level was driven by strong growth across Brisbane (1.0%), Adelaide (1.3%) and Perth (1.5%), whereas Sydney (0.2%) and Melbourne (-0.3%) recorded either soft growth or outright falls over the month.

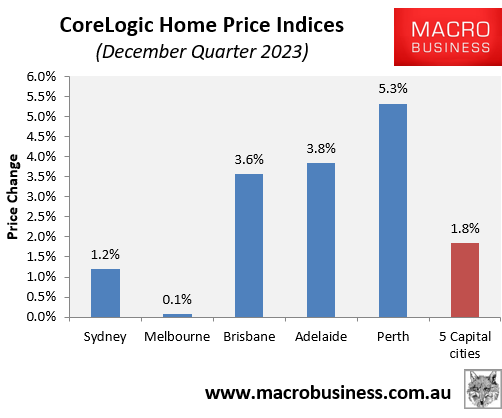

Quarterly value growth also moderated to 1.8% at the 5-city aggregate level.

But again, this growth was driven the Brisbane (3.6%), Adelaide (3.8%) and Perth (5.3%), whereas Sydney (1.2%) and Melbourne (0.1%) recorded only soft quarterly growth:

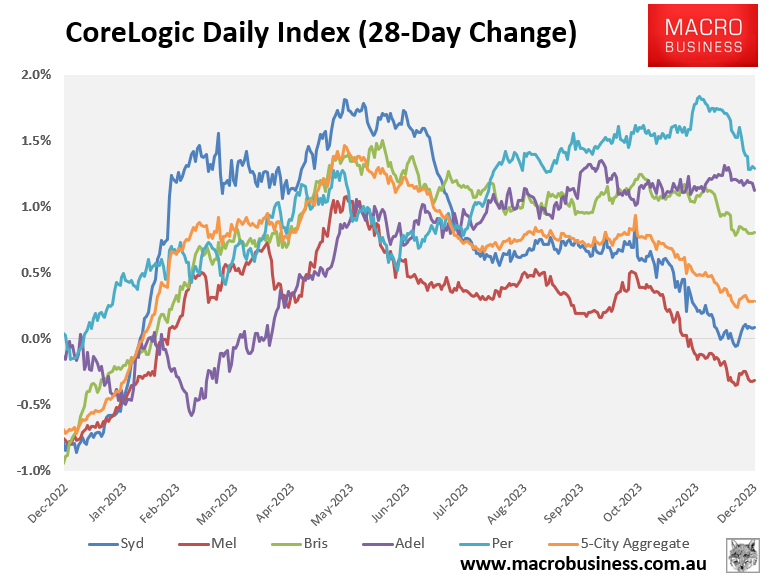

The next chart plots the 28-day price change across the five main capital city markets and shows how Australian house prices have turned two-speed:

The Reserve Bank of Australia’s (RBA) Melbourne Cup Day interest rate hike clearly stifled the momentum of Sydney’s and Melbourne’s housing markets, which has pulled value growth lower at the 5-city aggregate level.

By contrast, the other major capital city markets have been less impacted and continue to record strong value growth.

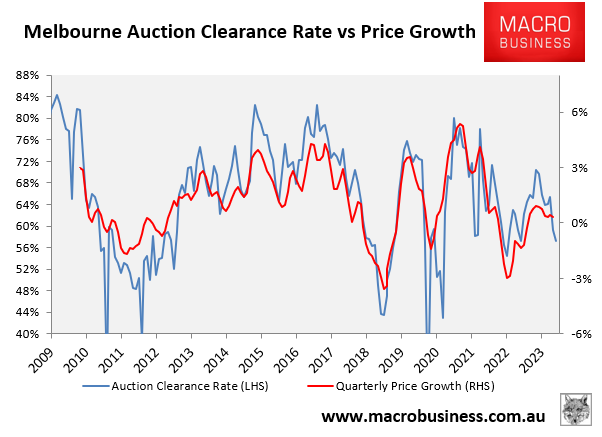

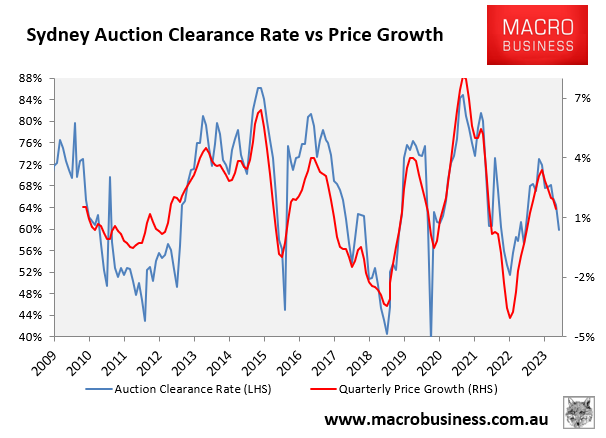

The above results have been reflected in the auction markets, which are dominated by Melbourne and Sydney.

Melbourne’s final auction clearance rate fell sharply towards the end of the year, from a peak of 70% in June to 57% in December:

Sydney’s final auction clearance rate has also fallen heavily, from a peak of 73% in May to 60% in December:

This suggests that a buyers’ market will develop for Sydney and Melbourne in early 2024, with outright price falls a distinct possibility.

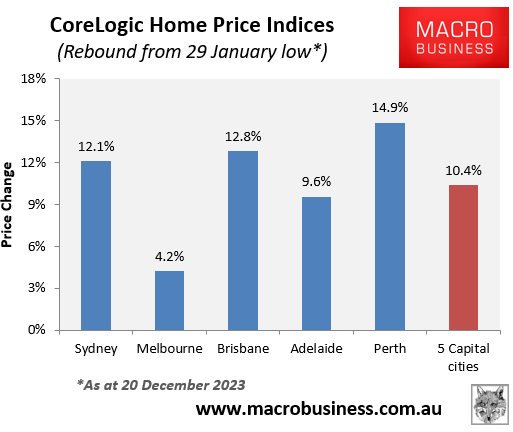

Finally, the next chart shows the extraordinary rebound in dwelling values since late January’s trough, despite ongoing rate rises from the RBA:

As you can see, prices rebounded strongly across all major markets with the exception of Melbourne, which recorded a modest rebound.

My guess is that dwelling values nationally will record sluggish price growth over 2024, dragged down by Sydney and Melbourne, but could begin to accelerate late in the year after the RBA commences an interest rate easing cycle.