The Australian retirement system is based on the presumption that the vast majority of people would own their homes.

However, due to dropping homeownership rates and people carrying mortgage debt well into their retirement years, that assumption is failing.

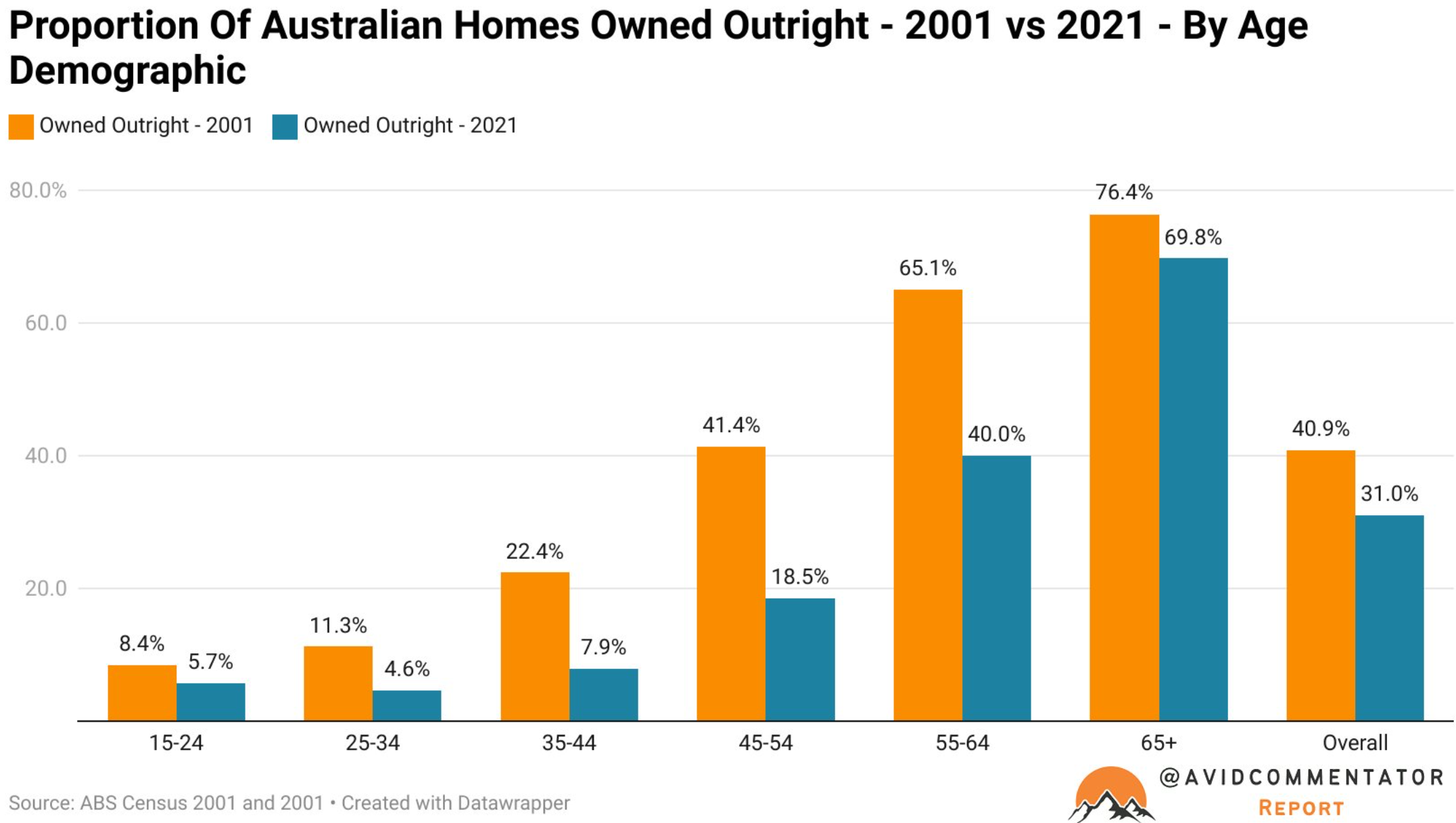

As shown in the next chart from Tarric Brooker, older Australians are carrying more mortgage debt into retirement (with significant increases in the 55-64 and 45-54 age groups).

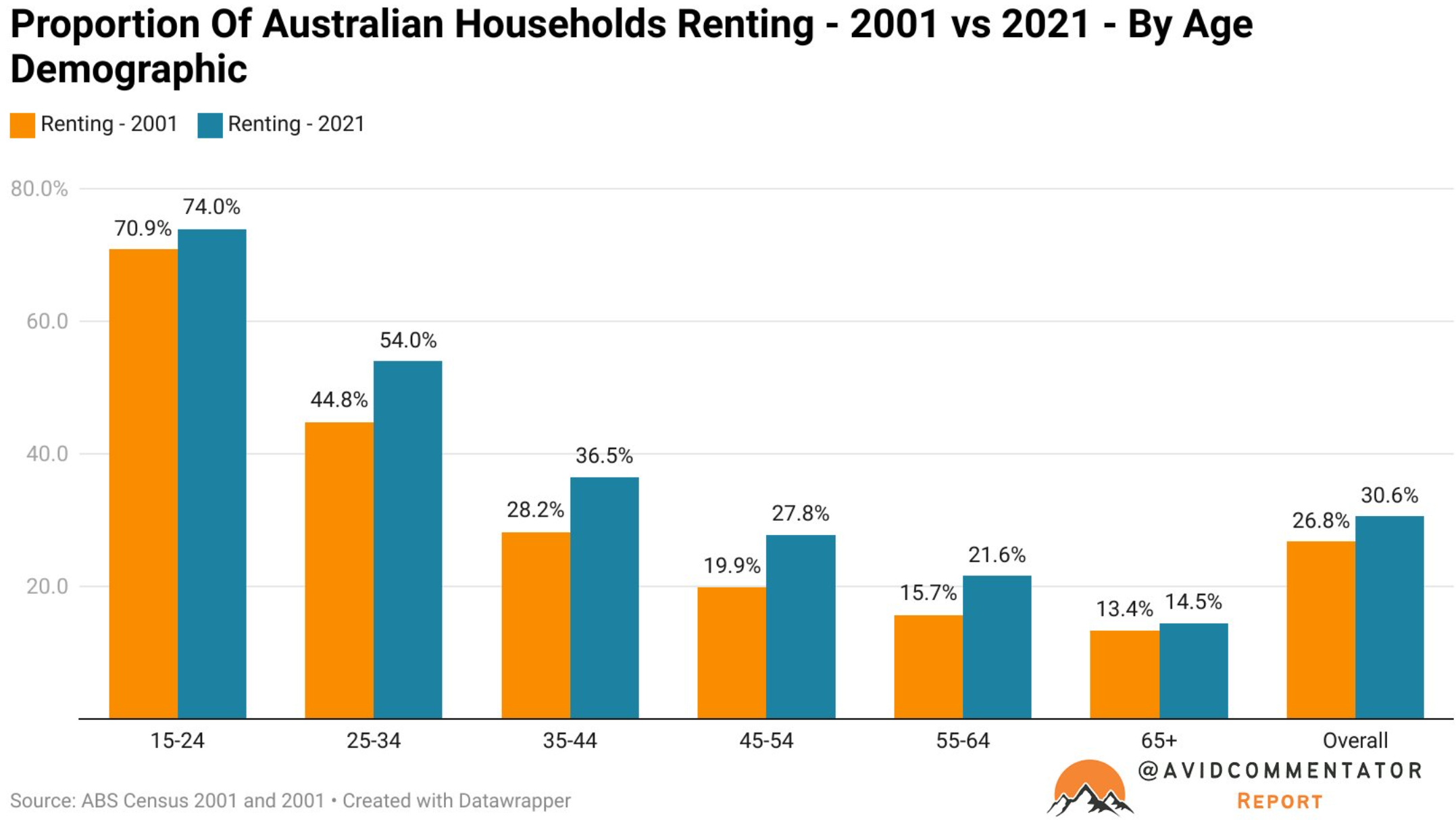

There has also been a corresponding rise in the share of households renting:

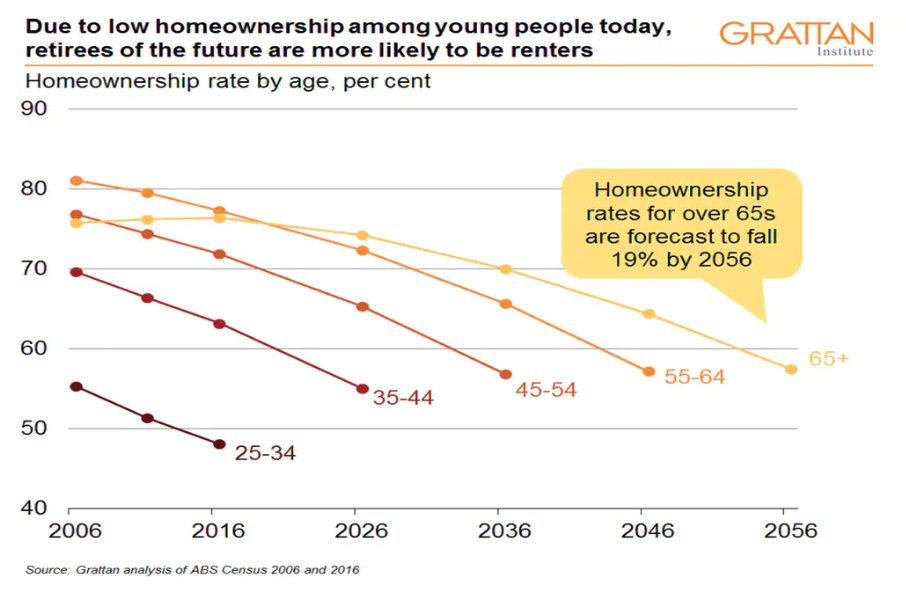

The Grattan Institute also projected that the share of people aged 65-plus who will own a home would decline from 76% now to 57% by 2056:

As shown above, less than half of low-income pensioners will own a home mid-century, down from over 70% today.

The nation’s worsening housing crisis and the sharp decline in home ownership rates risks blowing up Australia’s retirement system, according to new research from AMP.

According to an AMP poll of 1000 Australians aged 50 and over, only one in seven planned to be mortgage-free when they retired, and one in nine expected to have more than $250,000 in outstanding debt.

AMP retirement director, Ben Hillier, warned that more retirees burdened with debt will be vulnerable to interest rate changes, posing a difficulty in long-term financial planning:

“For as long as we can remember, the Australian dream has been debt-free homeownership, which provides the financial foundation and security for a comfortable retirement”.

“While home values and super balances are increasing, research shows that more and more Australians will be retiring with increasing levels of household debt”.

Harry Chemay recently posted in Michael West that rents will chew-up a higher share of retiree incomes, placing many in financial stress:

“It basically means: hitting retirement either as a renter or as a heavily indebted mortgagor is going to impact the retirement security of very many Australians, possibly putting pressure on both the Age Pension and superannuation system”.

“Whichever way governments of either persuasion slice or dice it, housing security and retirement security are two sides of the same coin”, Chemay said.

Put simply, future retirees in Australia will increasingly rent, whereas others will be saddled with growing levels of mortgage debt.

Both developments will place increasing strain on Australia’s retirement system.