This is amusing (and good for the east coast of Australia):

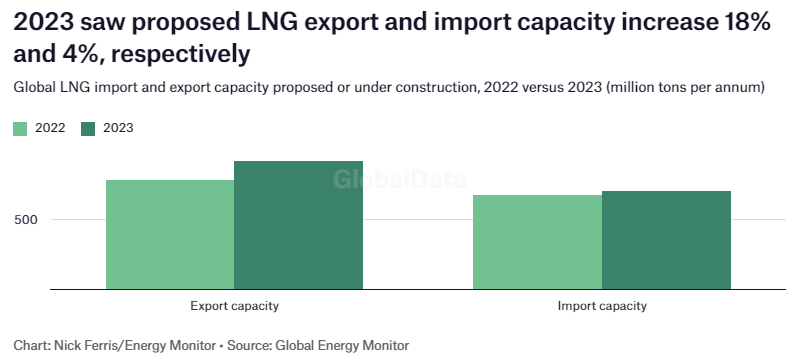

Analysts predict peak global gas demand, but the global LNG pipeline just keeps growing, threatening serious oversupply. LNG projects under development totalled 917 million tonnes per annum (mtpa) of new export capacity and 705mtpa of new import capacity at the end of 2023, according to the non-profit Global Energy Monitor. This represents an 18% and 4% year-on-year increase, respectively, and an estimated $1trn in investment.

The countries developing the most new export terminals are the US (336.9mtpa), Russia (164.1mtpa), Canada (75.8mtpa), Mexico (69.3mtpa) and Qatar (49mtpa).

China, India, Germany and Brazil are responsible for the most LNG import capacity under development.

Those figures are very exaggerated. They must include every proposed export project down to two horse towns.

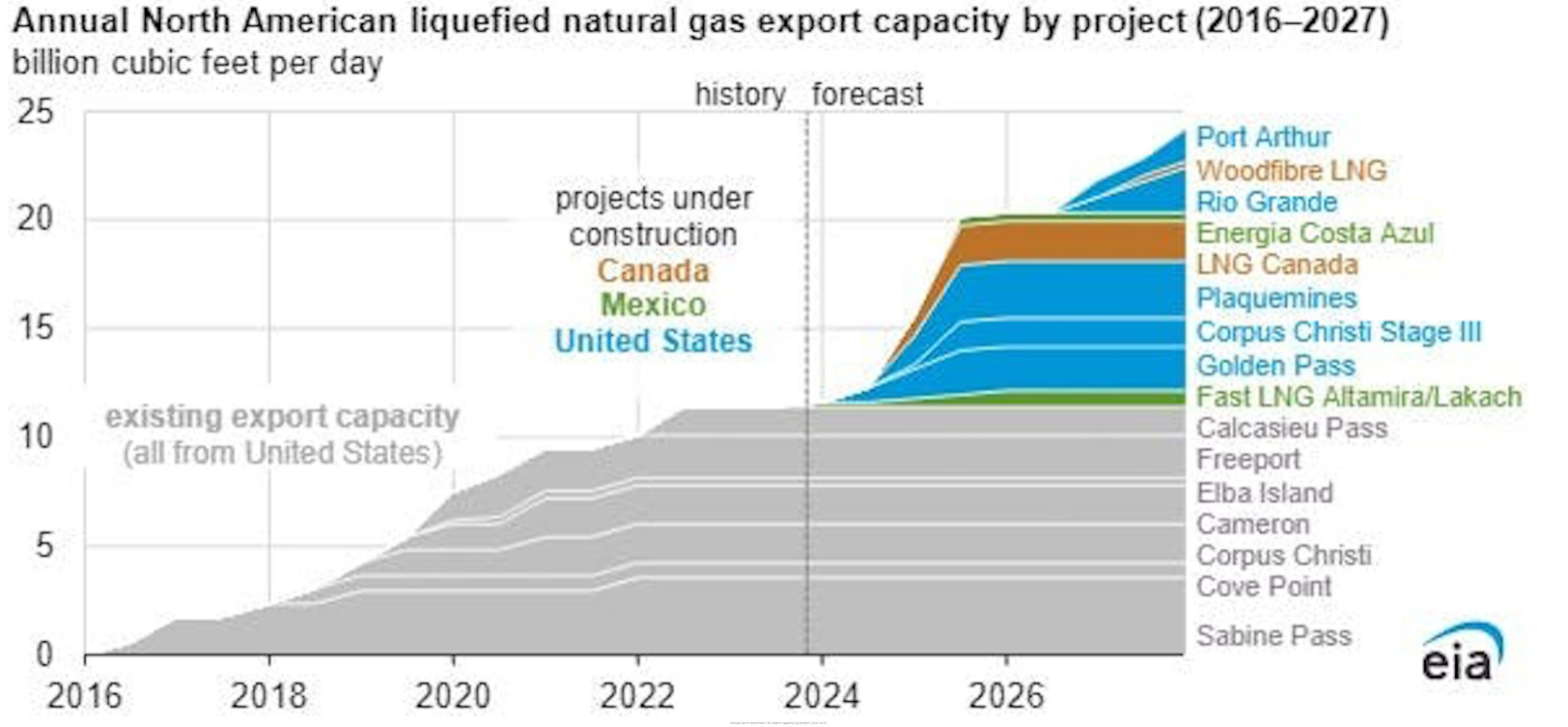

Still, the argument holds. North America alone will expand supply dramatically by 2028:

You can add roughly half that again from Qatar, Russia and Africa.

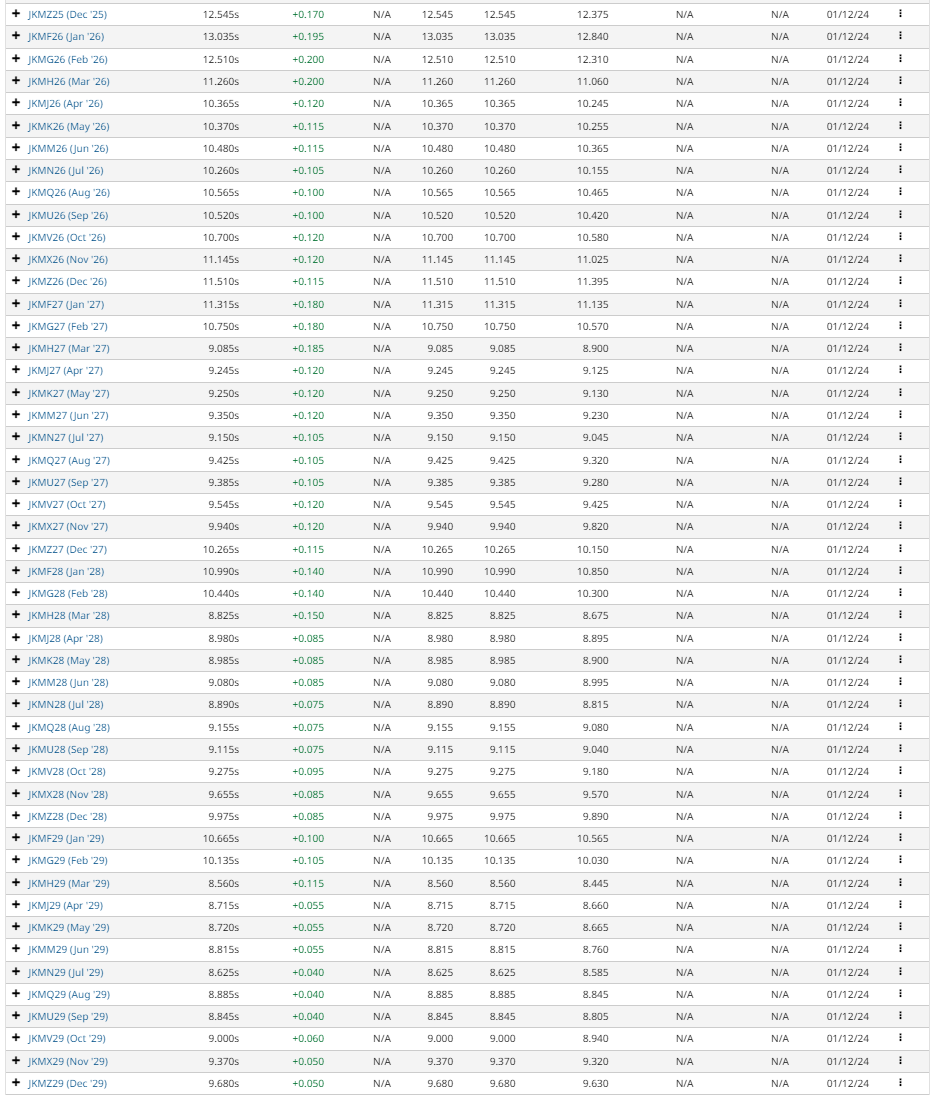

This glut is going to crash prices. For some reason, JKM futures have somewhat priced it but nowhere near low enough:

As happened in Australia, consolidation and writedowns will follow the capacity expansion and prices fall below cash cost for a time.

Such lower prices will aid the east coast power market so long as the government of day forces the gas export cartel into line.

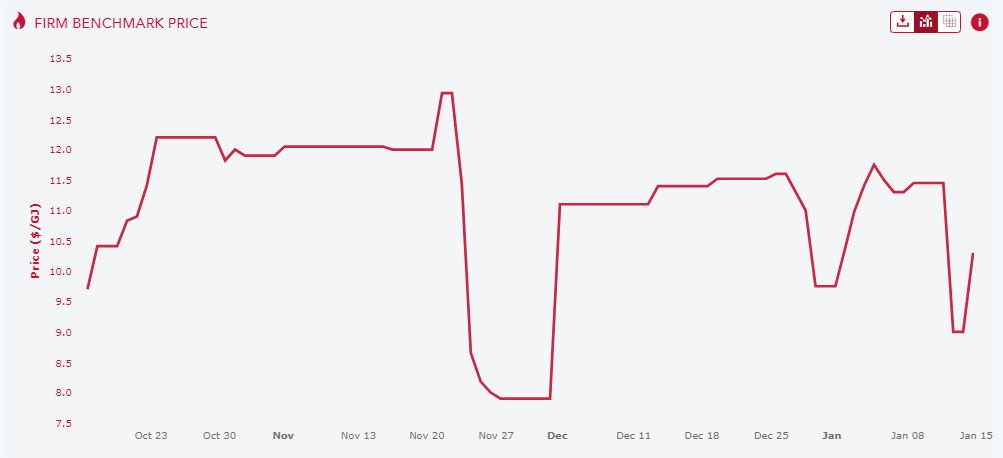

Prices have fallen recently with a lower JKM export net back, though that may be coincidence:

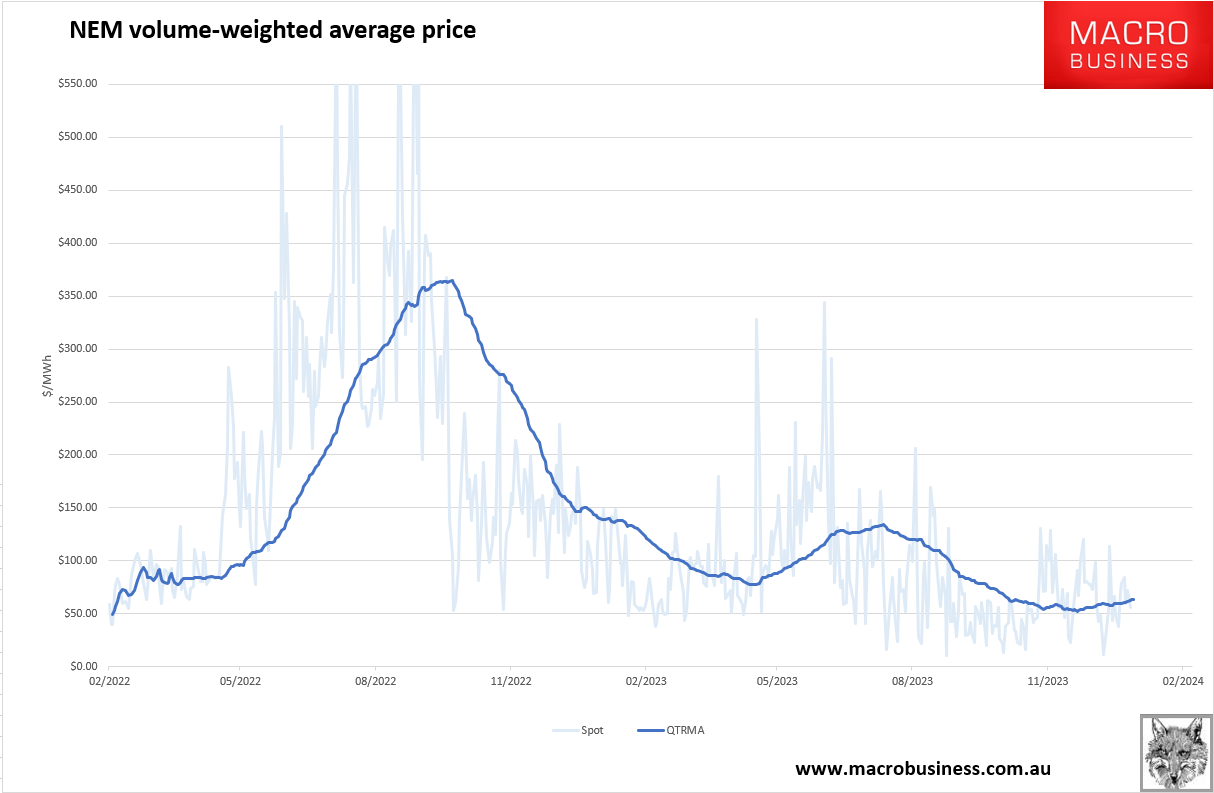

Bringing down wholesale power costs:

It is a never-ending demonstration of Aussie stupidity that we are better off when our gas export prices fall.