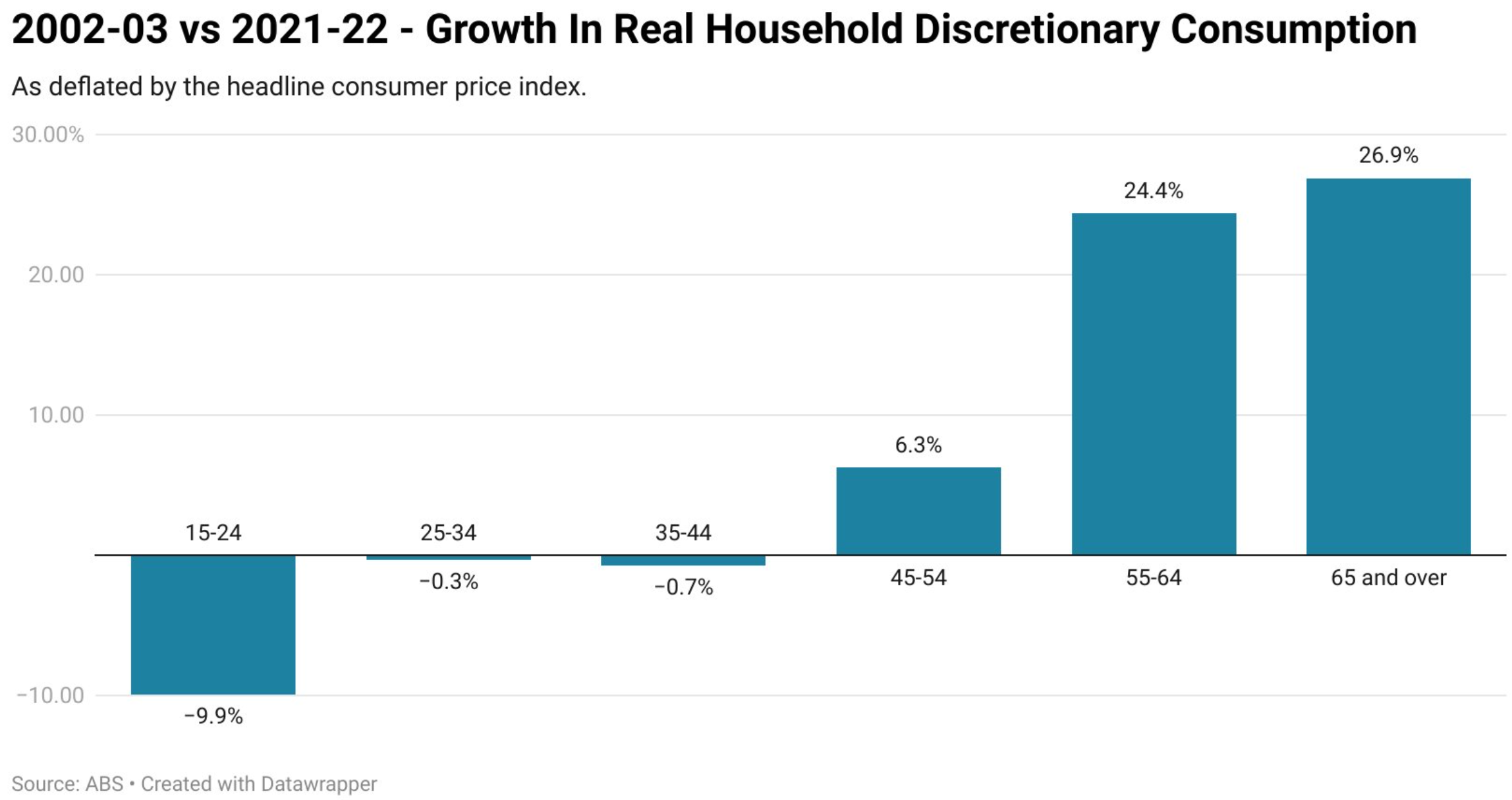

On Friday, I published data compiled by independent economist Tarric Brooker showing the massive divergence in spending by different age cohorts.

Source: Tarric Brooker

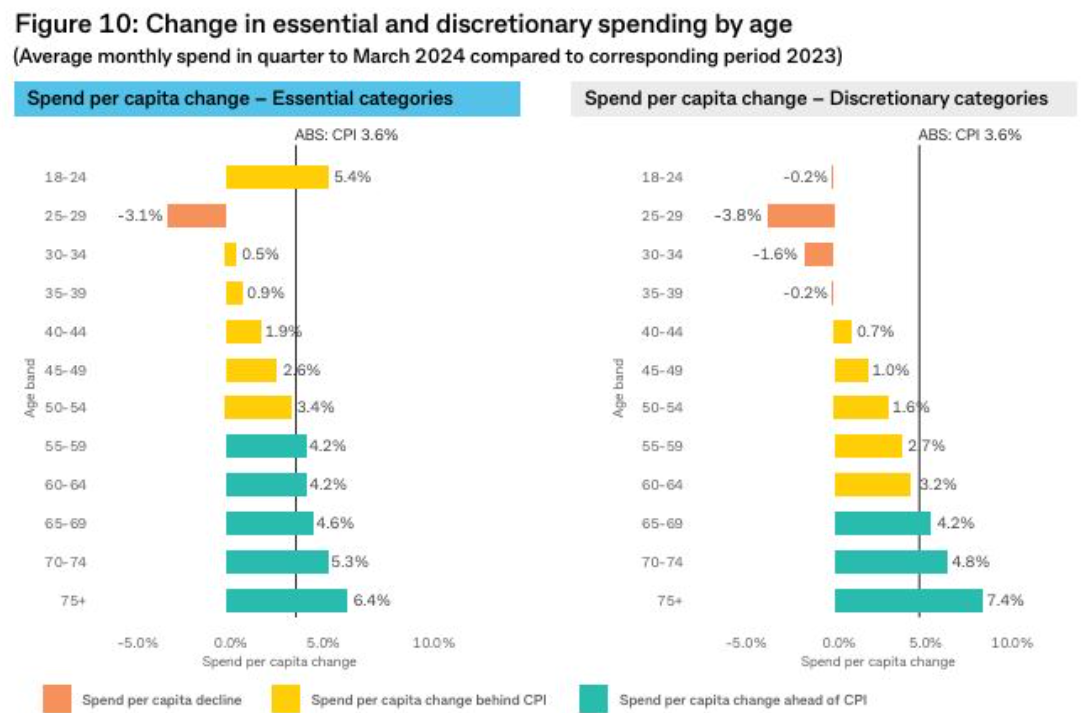

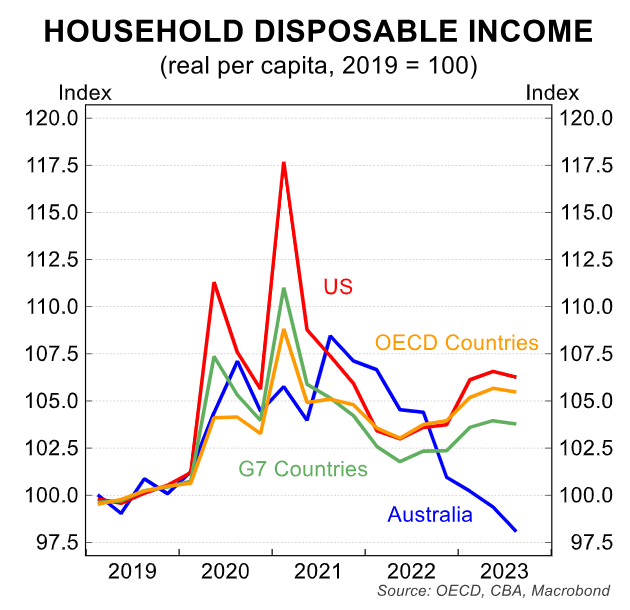

Brooker’s data shows that Australians under 45 cut their real discretionary consumption over the 19 years to 2021–22. And that was before inflation took off, which led to further spending cuts, as the CBA below illustrates:

By comparison, older Australians have increased their real discretionary consumption over the past two decades.

Over the weekend, The SMH’s business reporter, Colin Kruger, published an analysis showing similar results.

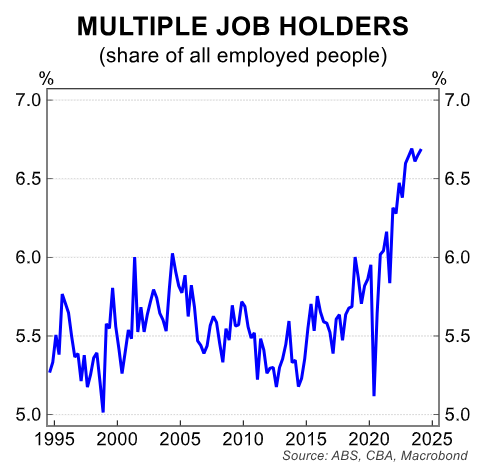

Kruger noted that calls to the National Debt Helpline have rocketed by 51% on 2022 levels “thanks to the twin poxes of high mortgage rates and grinding inflation, which shows people are struggling despite a record number of Australians now holding down two jobs”.

Callers to the Consumer Action Law Centre’s (CALC) Victorian helpline have also identified rising energy bills as one of the top three areas of financial difficulty.

“What is clear is that low-income households are being priced out of an essential service”, CALC chief executive Stephanie Tonkin says.

Even Anglicare in booming Western Australia reported that 68% of people using the charity’s emergency relief services are doing so for the first time.

Meanwhile, there is a large cohort of Australians that are unaffected by soaring mortgage repayments and rents who are spending up big.

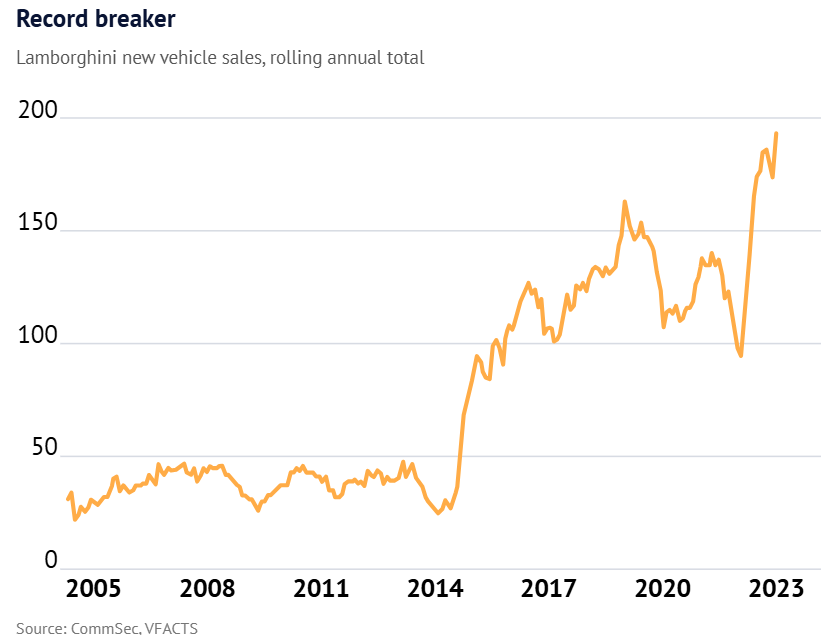

Kruger points to fact that sales of luxury Lotus, Lexus and Lamborghini vehicles hit a record high this year.

Spending on cruises also surged by 22% in the year to March 2024.

“We’ve never seen so much demand for expedition cruising from our clients”, remarked Travel Associates boss Rachel Kingswell.

Meanwhile, Flight Centre has recorded a 94% annual increase in business class flight bookings.

“[Baby Boomers] hold a disproportionate share of wealth and are now retiring and spending time travelling”, noted analysts from Jarden Securities.

The situation is best summed up with the below quote from Colin Kruger:

Wade Tubman, head of analytics at CommBank IQ, noted the seismic split between the cashed-up cohort of mortgage-free households – which makes up a third of the market – and the other two-thirds comprising renters and homeowners with a mortgage.

Owners with no mortgage increased their recreational spending by 14% in 2023. Mortgage holders and renters increased it by 3%, which means their spending went backwards in real terms…

So basically, the whole spending curve of the generations has flipped on its head.

As I noted on Friday, there are three faces of Australia’s economy.

The RBA’s 4.35% of rate hikes have directly impacted around one-third of owner-occupier mortgage-holding households, notably Generation Xers and Millennials with young children.

They have seen their mortgage repayments rise by about 50%, but their discretionary incomes have fallen at the fastest pace due to inflation and increased living costs.

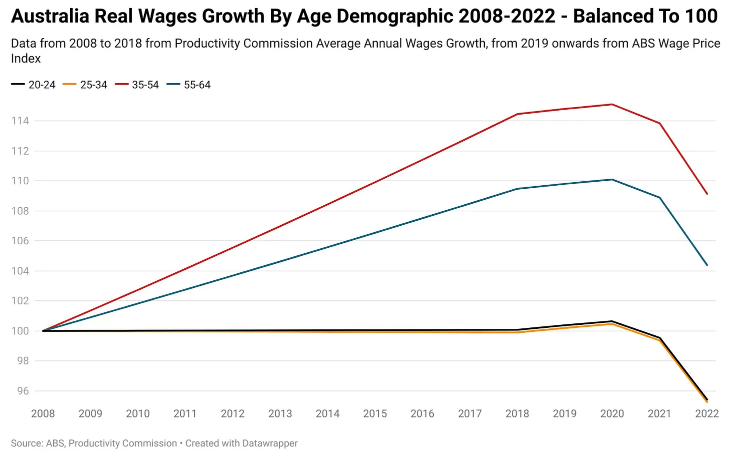

Tarric Brooker’s chart below shows that Australians under the age of 35 earn less in real terms than they did in 2008:

Chart by Tarric Brooker

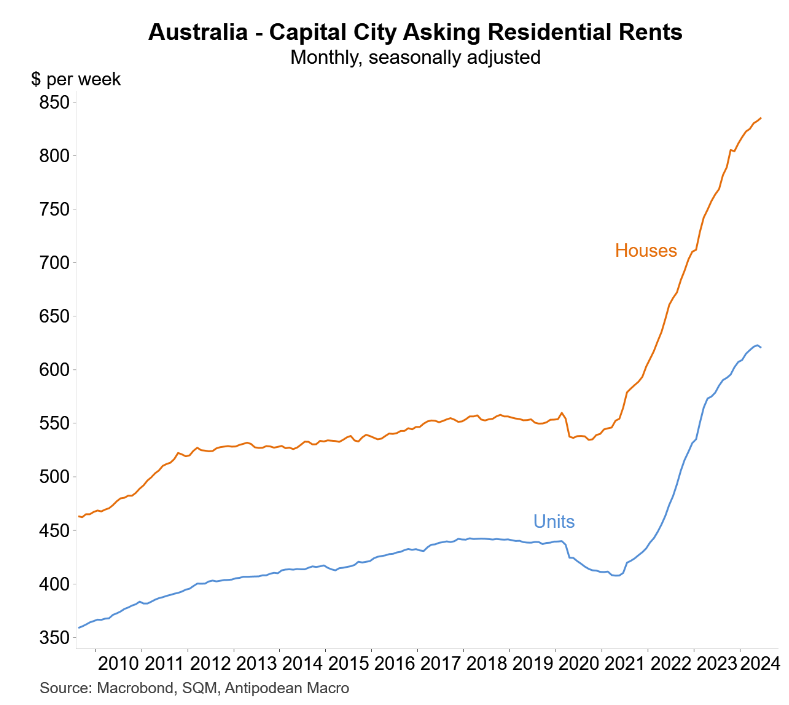

Hyperinflationary rents and declining real incomes have had a negative impact on another one-third of renting (primarily younger) households, which has lowered their discretionary spending.

The baby boomers lead the older generations at the opposite end of the spectrum.

They typically own their homes outright, so rising mortgage rates and rent hikes have little effect on them.

Some baby boomers are even benefiting from rising rents, as they own a major share of Australia’s investment properties (many of which are mortgage-free).

Most older Australians do not work. Therefore, income tax hikes owing to bracket creep do not affect them.

Australians receiving the old age pension also have their payments linked to inflation (unlike workers’ incomes). Therefore, their buying power has generally been preserved.

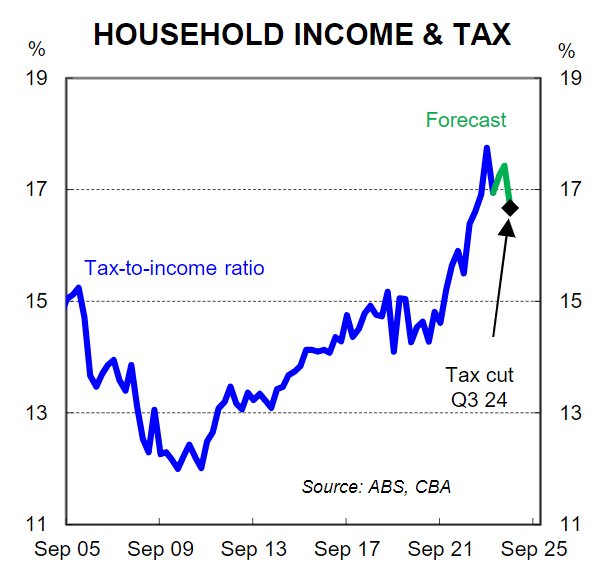

The data above show why Australia urgently needs tax reform that shifts the base away from productive activities (i.e., taxing work) and towards more efficient sources like resources, land, and consumption.

Australia’s tax system is unsustainable, inefficient, and inequitable because it is based on a shrinking proportion of workers.

By contrast, the proportion of taxes collected through indirect channels (such as GST and fuel excise) is decreasing.

This is especially true considering that the share of elderly Australians is increasing and paying fewer taxes than before, despite possessing the majority of Australia’s wealth.