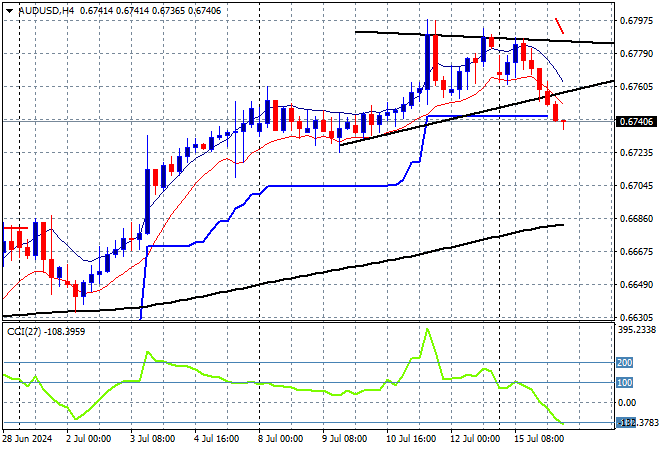

A mixed session on Asian markets with last night’s meagre lift on Wall Street not translating to further confidence in the region, with a much firmer USD not helping. Bond markets are selling off, indicating a potential Trump 2.0 win in November with the Australian dollar off from its six month high as it retraces down towards the 67 cent level.

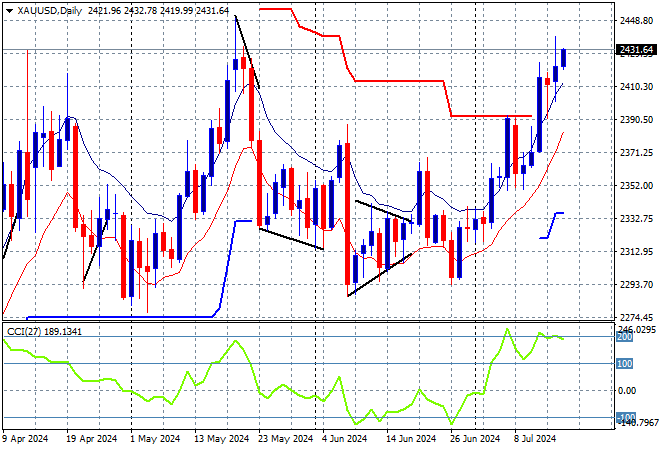

Oil prices have slipped again with Brent crude almost retracing below the $84USD per barrel level while gold is trying to match its previous high, currently floating above the $2430USD per ounce level:

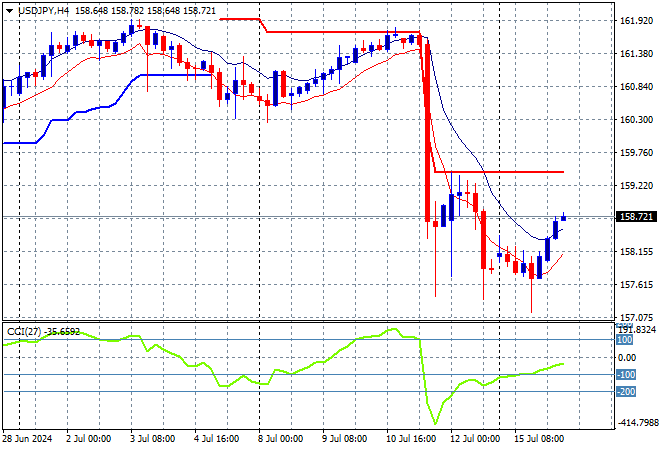

Mainland Chinese share markets are still flat in reaction to yesterday’s GDP print with the Shanghai Composite down a handful of points while the Hang Seng Index is off again as it fails to gain momentum, down more than 1% to 17756 points. Meanwhile Japanese stock markets reopened after their long weekend holiday with the Nikkei 225 closing some 0.4% higher at 41331 points while the USDJPY pair has made a small leap higher to almost get above the 159 level as the USD strengthens across the board:

Australian stocks were unable to advance but the ASX200 was able to stay above the 8000 point level, closing at 8007 points while the Australian dollar has dropped below its Friday night finishing position and could threaten the 67 cent level next as momentum flat lines:

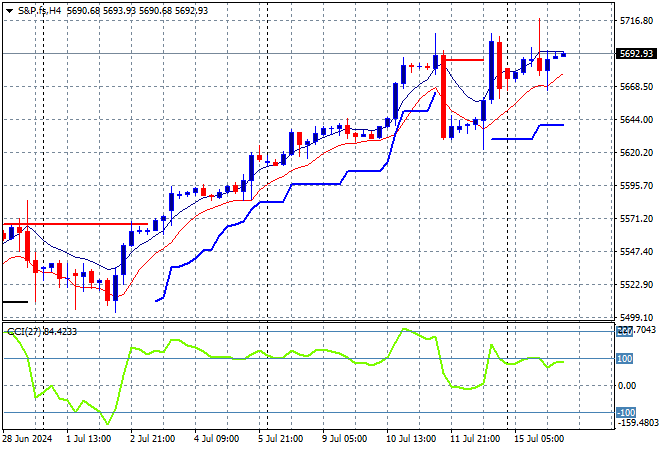

S&P and Eurostoxx futures are relatively flat as we head into the London session with the S&P500 four hourly chart showing price action hesitating around the point of control at the 5700 point level with volatility rising:

The economic calendar ramps up with the closely watched German ZEW survey, then US retail sales plus more earnings releases.