The Reserve Bank of New Zealand this week left the official cash rate on hold at an overly restrictive 5.50%.

However, in its commentary accompanying its decision, the Reserve Bank took a dovish view, suggesting that it is preparing to cut rates in the near future.

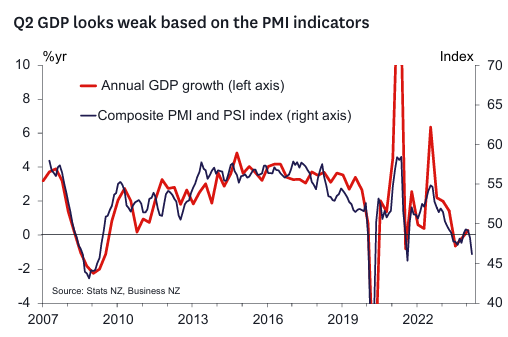

In particular, the Reserve Bank noted that New Zealand’s forward growth profile and the labour market have weakened:

“Recent higher frequency indicators suggest that near term growth in business activity has weakened. A range of business and consumer surveys, and higher frequency spending and credit data, all point to declining activity”…

“Recent survey measures of hiring intentions and job vacancies indicate flat employment levels”.

This suggests that the Reserve Bank will downwardly revise its forecasts for the economy in the August Statement, in turn lowering its CPI inflation forecasts.

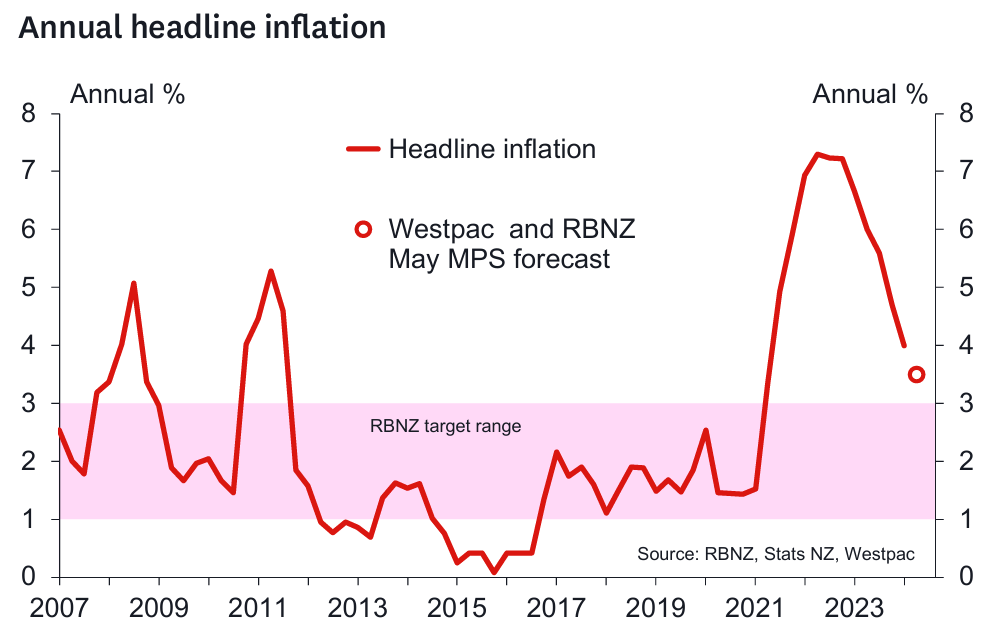

Indeed, the Reserve Bank on Wednesday sounded more confident on inflation, noting that it expects it to return to its target range “in the second half of the year”.

It also noted that “growing excess capacity in the domestic economy provides greater certainty that [domestic inflation measures] will sustainably decline”.

Overall, the commentary suggested that the Reserve Bank is preparing to pivot to an easing bias, possibly as early as its August meeting. Although this will be contingent on compliant Q2 CPI and labour force reports, which are due in the coming weeks.

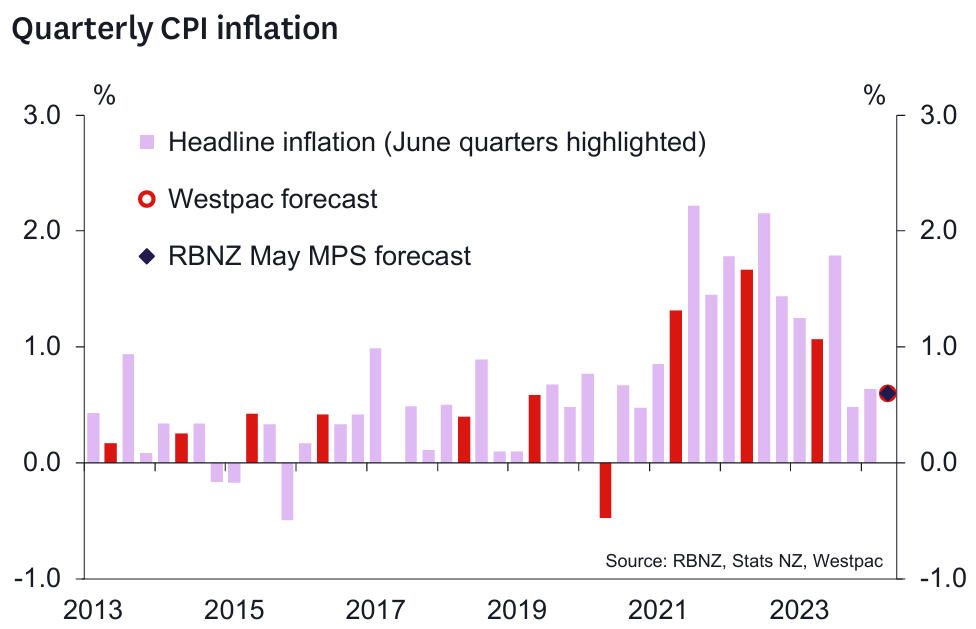

Separately, Westpac estimated that New Zealand consumer prices rose by 0.6% in the June quarter. This would see the annual inflation rate fall to 3.5%, down from 4.0% in the March quarter.

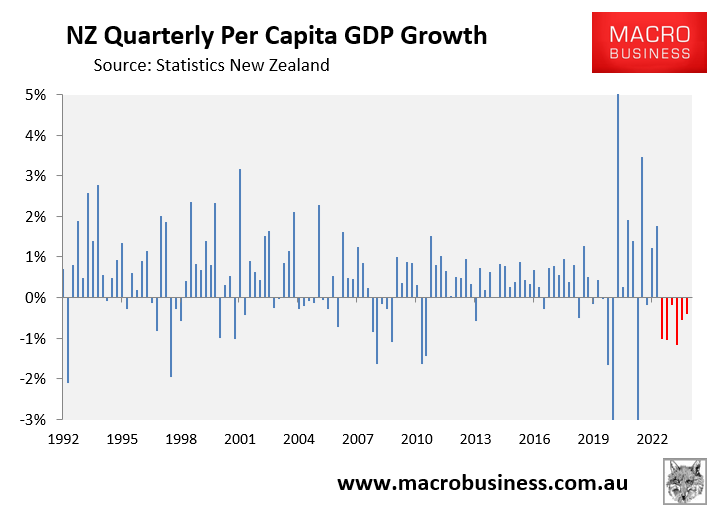

The Reserve Bank needs to tread cautiously given that New Zealand’s per capita GDP has already collapsed by 4.3% from the late 2022 peak, following six consecutive quarterly declines:

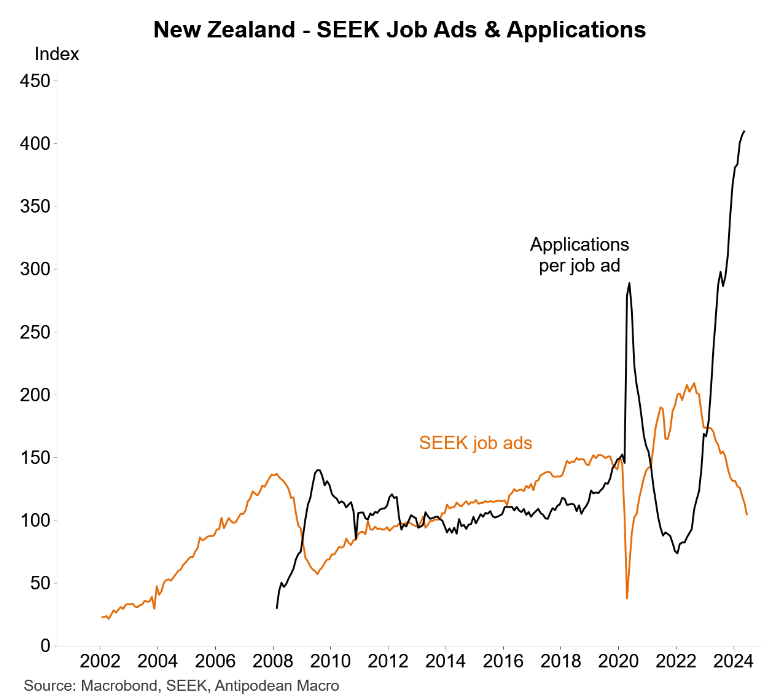

Job ads have also collapsed and applications per job ad have soared, pointing to sharp rises in unemployment and underemployment:

The Reserve Bank’s decision to hold the cash rate at 5.5% will ensure that the recession deepens.