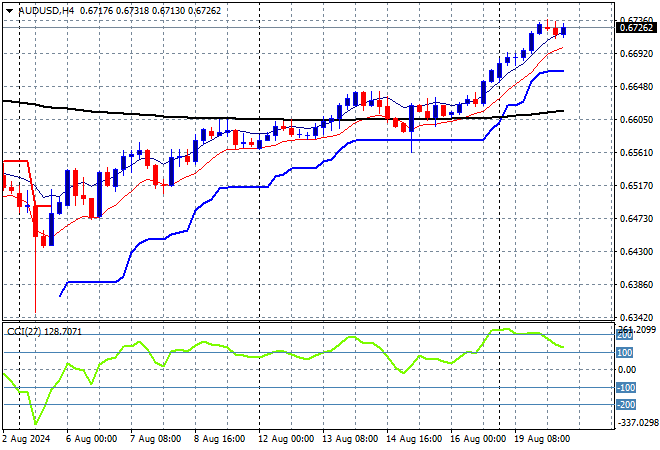

Another relatively solid session for Asian share markets although Chinese equities are having another rough ride as the PBOC leaves lending rates alone while the latest RBA minutes didn’t give any further evidence of what was going on. Futures for Europe and Wall Street are a bit flat going into tonight’s session without much on the calendar with the USD still on the backfoot versus Euro and other currencies with the Australian dollar looking a lot stronger as it lifts beyond the 67 cent level.

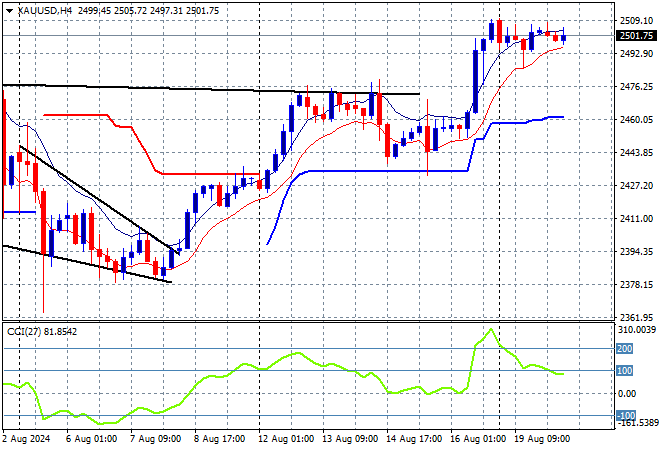

Oil prices are losing further short term momentum as Brent crude retreats below the $77USD per barrel level while gold is holding on to its breakout above the $2500USD per ounce level:

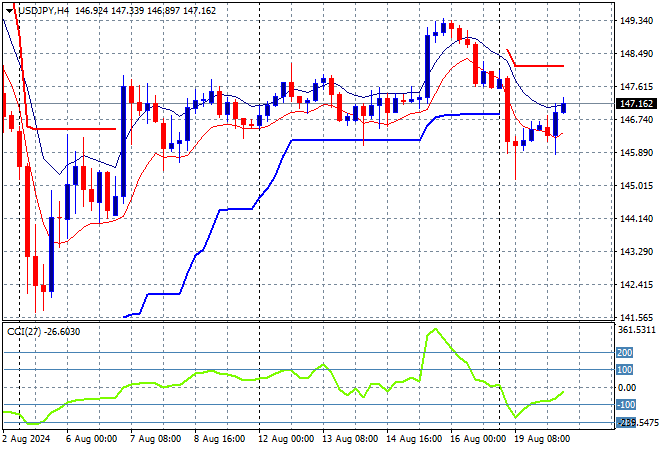

Mainland Chinese share markets slumped again after recently finding traction with the Shanghai Composite down nearly 1% going into the close while the Hang Seng Index is also off, currently down 0.5% to 17480 points. Meanwhile Japanese stock markets are getting hectic again on Yen volatility with the Nikkei 225 closing nearly 1.8% higher to 38062 points while trading in USDPY has seen a big lift back above the 147 handle after previously threatening the 145 level:

Australian stocks eked out another small gain with the ASX200 lifting just 0.2% to almost close above the 8000 point level while the Australian dollar was able to hold on to its move above the 67 cent level:

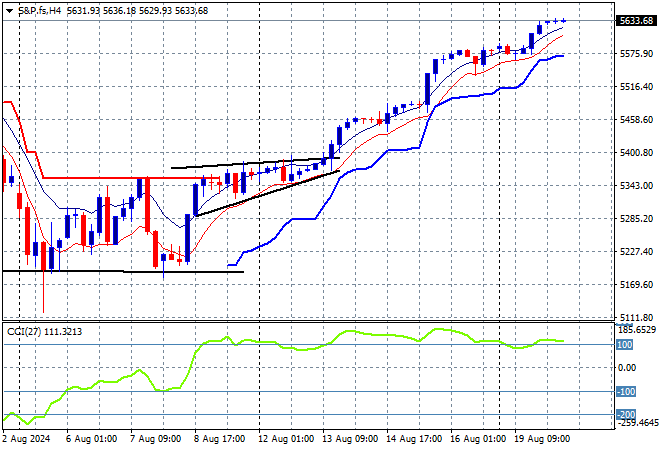

S&P and Eurostoxx futures are barely tracking higher going into the London session with the S&P500 four hourly chart showing continued further upside returning to the major index following the recent breakout which still has nice momentum behind it:

The economic calendar ramps up with the latest Euro core inflation print, then quite a few Fed member speeches to keep an ear out for.