ANZ and Westpac are debating why the RBA has no idea what it is doing.

The former says that the RBA is wrong on the neutral rate of inflation being around 4.5%.

Wages growth has slowed across awards, enterprise bargaining agreements and individual arrangements, pointing to a broad-based slowdown.

Indeed, if we consider lags between the unemployment rate and wages trends, the ‘natural rate’ of unemployment [NAIRU] could be closer to 3.75 per cent.

OK, Westpac examines why it might be lower than the bank thinks.

[The RBA] model starts from the presumption that prices are a (roughly stable) markup over costs, including labour costs. A bit of algebra later leads to a relationship that states that wages growth minus productivity growth is approximately equal to inflation (prices growth).

The deeper question is: with wages growth tracking in the low 3s and productivity growth not being zero, why has the RBA focused so much on the risk that wages growth is unsustainable?

I can’t help thinking that this partly reflects deep-seated narratives about the Australian economy not being competitive. These narratives stemmed from the so-called ‘real wage overhang’ that emerged in the 1970s following the policy-induced wages breakout then.

Another bout of this belief system emerged after the mining boom and attendant strong income growth.

Since then, restoring competitiveness by crimping wages growth has been a common go-to in the policy discourse in Australia, far more than elsewhere in my observation.

It is as if people forget that exchange rates tend to move much faster than domestic labour costs.

In any case, even if productivity growth averages a touch lower than 1% (worse than recent history), then by the RBA’s own figuring, WPI growth averaging 3.2% (the annualised rate of the past three quarters) is well and truly consistent with inflation averaging 2½% or below.

Right you are.

But let’s face it. As smart as these bank economists are, they are not in a very good position to call a spade a spade.

As MB has argued for a decade, in a labour market growth-led economy—which can also be called an immigration-led economy—there is no sustainable wage growth.

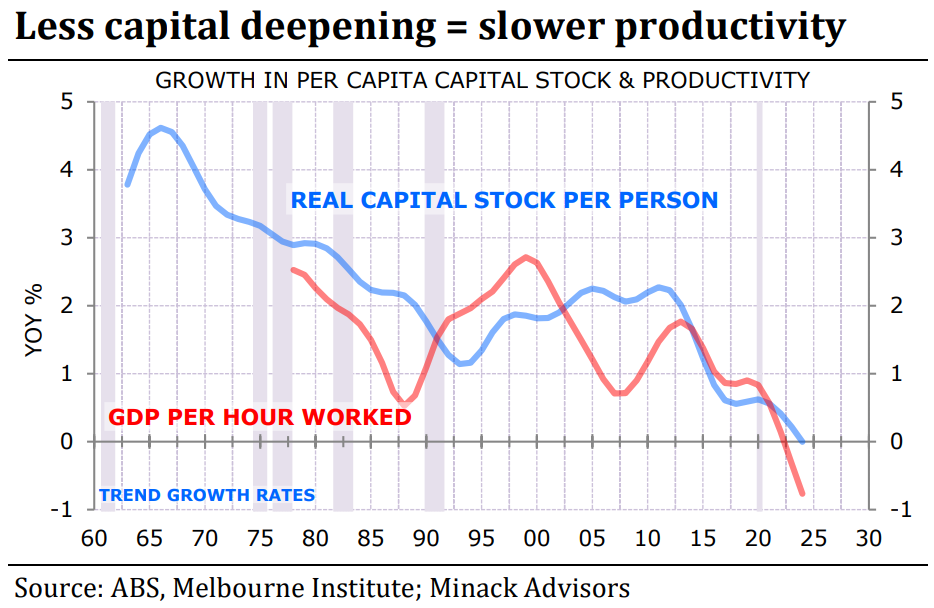

The capital side of the economy is always behind demand—that is, it is shallowing—which kills productivity.

At the same time, the labour side of the economy is in a permanent supply shock, meaning there is no labour pricing power to muscle up wages, so they fall as well.

Rentier profits are boosted via population growth, not productivity, so there is no dividend for workers and no inflation either.

Wherever this economic model has been adopted, the result is the same.

The RBA changed its leader when Phil Lowe stuffed this up for nearly a decade:

However, the new leader did not change its outmoded classical economics thinking.

This is not a 70s hangover. It’s woke drunkenness.

In the absence of a primary growth driver—like mining (China) or government stimulus (COVID) or something else—mass immigration kills all three of productivity, wages and inflation.

The NAIRU in this economy is very likely below 3% unemployment and may well be below 2%.

The RBA is repeating precisely the same mistake it did pre-COVID because it is not allowed to think about immigration.