Last night saw the release of the latest US Fed Minutes with the fallout from Trump’s new Treasury secretary appointment still pushing the USD lower. Wall Street lifted slightly to almost make a new record high, helped along by small caps while European shares were able to put in small gains as well. Most currencies gapped higher over the weekend against USD with Euro lifting straight through the 1.05 handle before giving up some gains overnight while the Australian dollar had a similar trajectory before stumbling back more than 50 pips to finish slightly above the 65 cent level this morning.

US bond markets saw some strong buying across the curve with 10 year Treasury yields falling more than 14 points down to the 4.2% level while oil markets pulled back on continued Middle East volatility as Brent crude was pushed below the $73USD per barrel level. Gold was also under the pump with another retracement well below the $2700USD per ounce level.

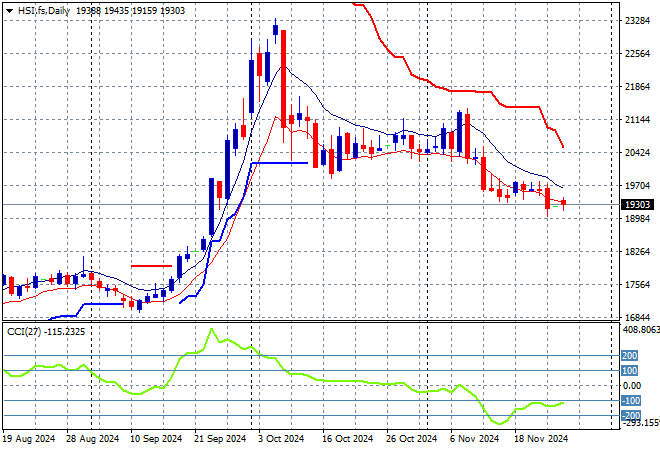

Looking at markets from yesterday’s session in Asia, where mainland Chinese share markets were falling going into the close with the Shanghai Composite down nearly 0.5% at one stage, finishing just 0.1% lower yet remaining below the 3300 point level while the Hang Seng Index was down around 0.4% to almost cross below the 19000 level.

The Hang Seng Index daily chart shows how short term resistance was finally being pushed away with a huge breakout above the 19000 point level that then set up for a run at the 20000 level in the response to PBOC stimulus. Price action is again bunching setting up for another potential breakdown if short term support breaks:

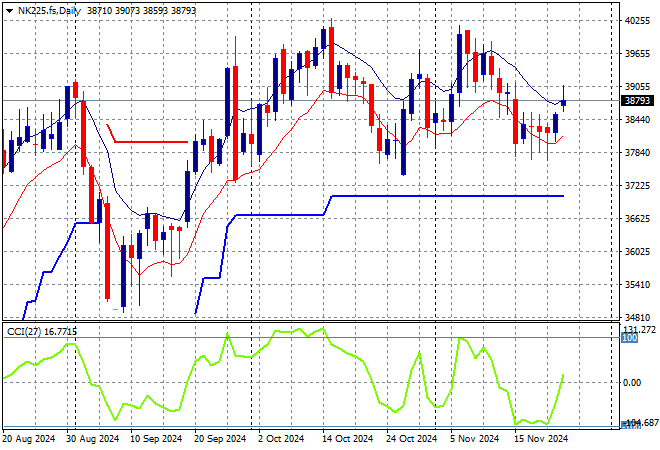

Japanese stock markets were the best performers however with the Nikkei 225 closing 1.4% higher to 38829 points.

Price action had been indicating a rounding top on the daily chart with daily momentum retracing away from overbought readings with the breakout last month above the 40000 point level almost in full remission. Yen volatility remains a problem here, with a sustained return above the 38000 point level from May/June possibly on the cards but positive momentum is not yet building.

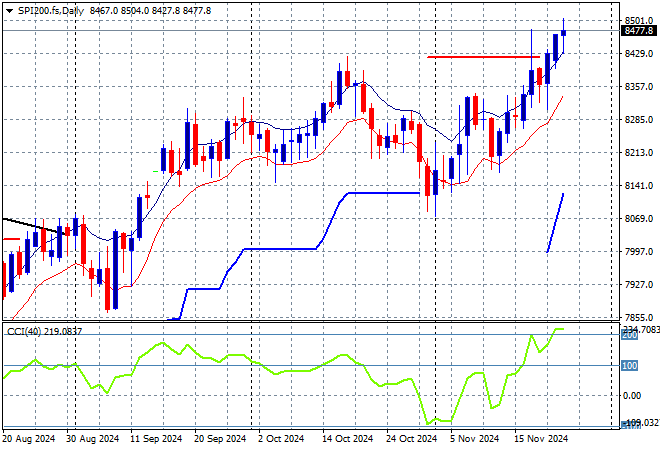

Outside of China, Australian stocks were the worst performers in the region as the ASX200 looks set to close just 0.4% higher at 8434 points.

SPI futures are up more than 0.3% following the small bounce on Wall Street overnight. The daily chart pattern was potentially signalling a top as short term price action suggests a return to the pre election uptrend, with the lower Australian dollar helping as we head straight into a Santa Rally but daily momentum is at extreme overbought levels:

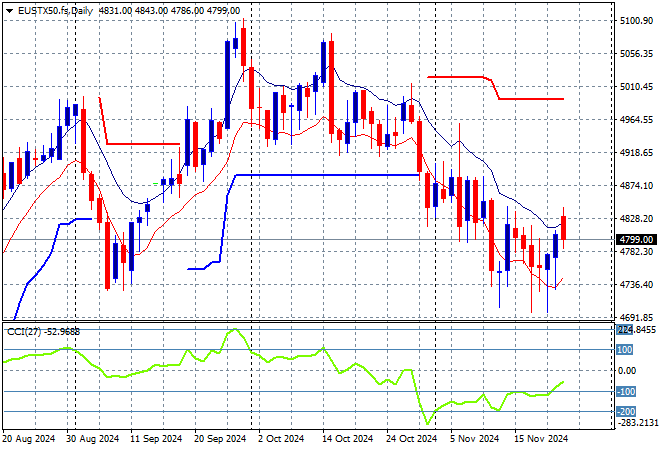

European markets had solid if not very impressive results across the Atlantic overnight with the Eurostoxx 50 Index closing nearly 0.3% higher to finish at the 4799 point level.

This was looking to turn into a larger breakout with support at the 4900 point level quite firm with resistance just unable to breach the 5000 point barrier. Price had previously cleared the 4700 local resistance level as it seeks to return to the previous highs but momentum is still oversold despite the positive Friday finish with price action still below previous support:

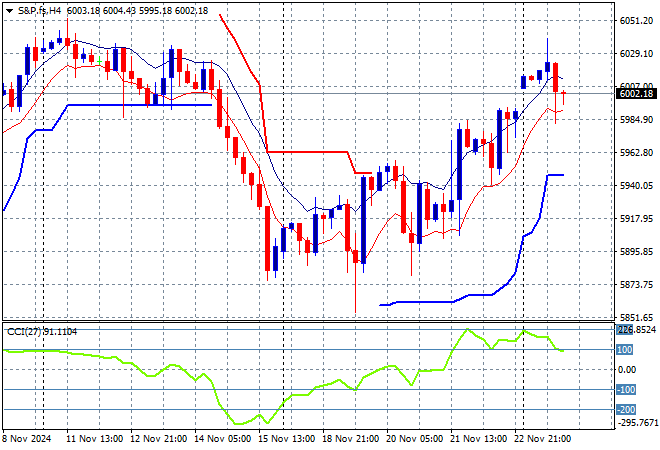

Wall Street had similar results as they continue to absorb the clown picks in Trump’s cabinet although the latest Treasury secretary pick has calmed things a little with the NASDAQ up just 0.2% while the S&P500 put on nearly 0.3% to finish at 5982 points and still on its way to another record high.

Price action is still looking extremely positive as all the stops will literally be taken out of business regulation, taxation, competition etc in a new dominating GOP Congress with the sky the limit here for big business – and with the Fed cutting rates, add more to the punchbowl. Watch short term support here at the 5940 point level however:

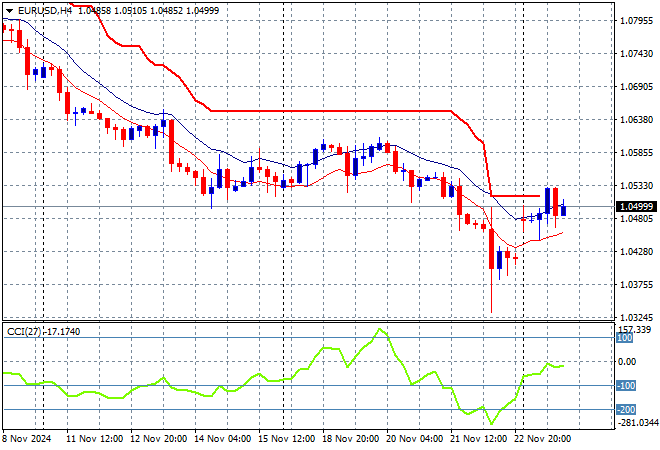

Currency markets had a wild reaction over the weekend Middle East ceasefire and US political news with a big gap against USD across the complex. This is shown clearly with Euro with a 100 pip reversal as it returned above the 1.05 handle after a volatile Friday night session that saw it almost dip to the 1.03 level.

The union currency had been pushed higher after remaining oversold for weeks in a dominant downtrend, then cleared overhead resistance at the mid 1.08 level in the lead up to the election. However last week saw a mild pause before a late selloff that despite the big weekend gap higher is not yet near those former levels as I contend we are still likely on our way back to parity as traders start to price in the now very unclear future for the continent:

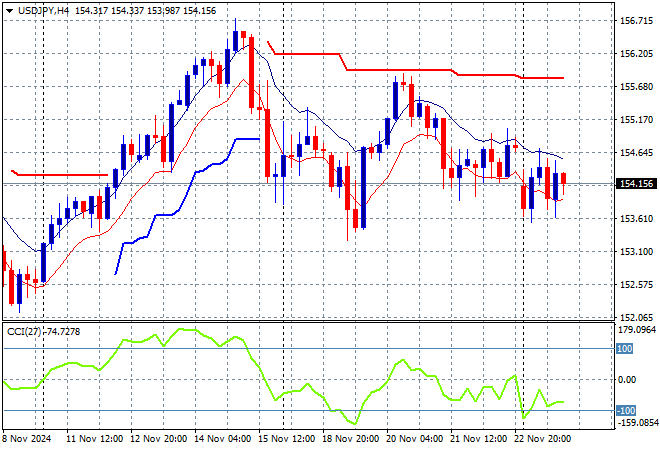

The USDJPY pair is getting close to retracement mode, testing the 154 handle on the weekend gap as USD weakens on the Treasury secretary news but Yen is still holding here just above the previous weekly low.

Short term momentum is still negative with price action unable to make new short term highs so this is setting up for a potential breakdown here below the 154 level in the coming sessions:

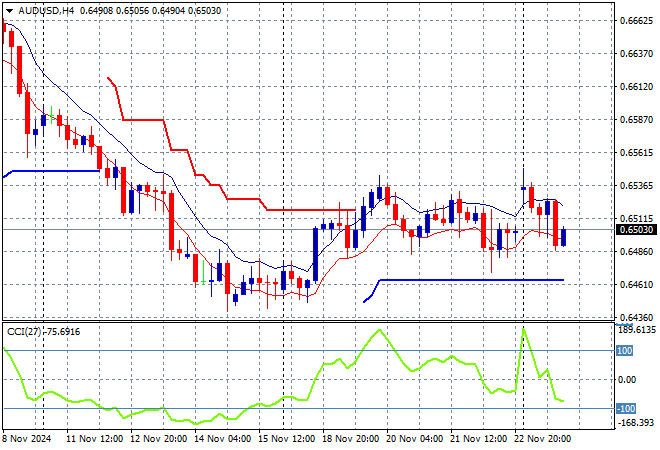

The Australian dollar had been one of the more robust undollars through the US election volatility but it still fails to make any further headway due to global macro concerns despite the weekend gap higher, remaining stuck at the 65 cent level.

The Pacific Peso could come under more pressure here on reweighting risks and the lack of action from the RBA as it wants to hold through to Feb/March next year, and this move had been already with a retracement back to the 64 handle most likely next:

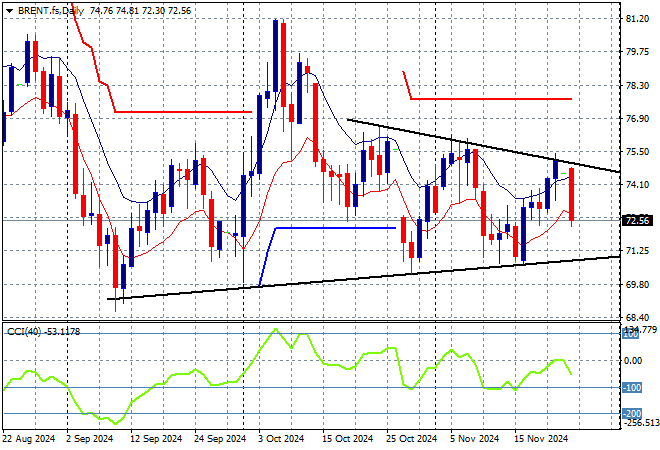

Oil markets are building again in volatility in the post US election tensions and potential peace talks/ceasefires in the Middle East as Brent crude was pushed strongly below the $73USD per barrel level overnight as the daily chart pattern continues to tighten like a spring.

Short term momentum remains in negative territory as medium term price action still supports a downtrend with my contention of another sharp retracement forthcoming if the $70-72 zone is not defended:

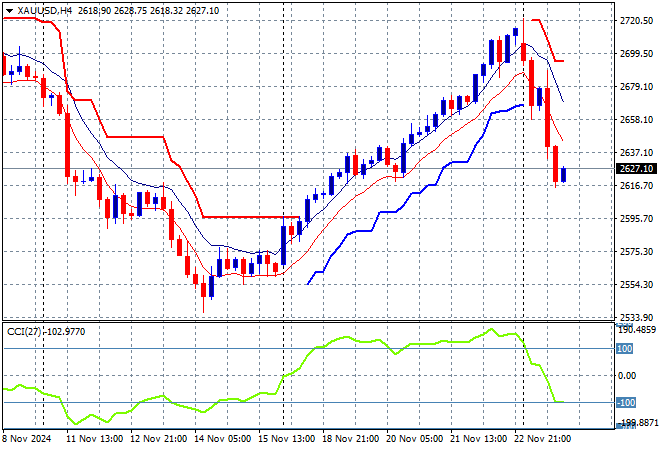

Gold had suffered the most out of the undollars with a swift selloff down below the $2700USD per ounce level from Friday night after the Treasury news, in line with the bond buying frenzy that could follow through below the $2600 level.

Price action had been accelerating in confidence as new levels of support were being created for the shiny metal regardless of USD strength but this pullback and rebound both are fighting too much around the $2700 zone so I’m skeptical of a new breakout here:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out/wrong on your position, so cry uncle and get out!