The final trading week is still looking a lot like Christmas with Wall Street continuing its Friday night bounceback on Friday while European stocks slid back as markets start to quieten down over the Xmas break. The latest US consumer confidence figures weren’t impressive but King Dollar fought back against the relatively mild fightback from the undollars from Friday, which saw Euro held back at the 1.04 handle again while the Australian dollar still can’t escape its trajectory and remains flat at the 62 cent level.

US Treasury 10 year yields pushed higher on the consumer confidence data, up 6 points to well above the 4.5% level while oil markets are trying hard to stabilise as Brent crude fell back to the $72USD per barrel level. Gold is still under the pump as it tries hard to remain above the $2600USD per ounce level after its recent $50 plus move lower and was largely unchanged.

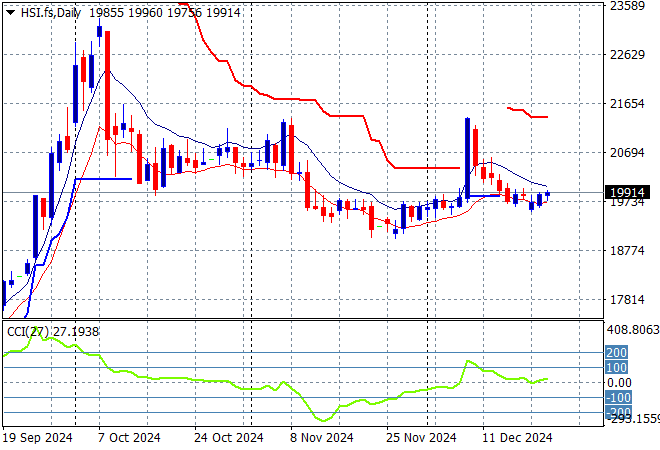

Looking at markets from yesterday’s session in Asia, where mainland Chinese share markets were having a wayward session with the Shanghai Composite up at the lunch break before closing more than 0.5% lower to 3351 points while the Hang Seng Index went the other way, advancing more than 0.8% to close at 19883 points.

The Hang Seng Index daily chart shows how short term resistance was finally being pushed away with a huge breakout above the 19000 point level that then set up for a run at the 20000 level in the response to PBOC stimulus last month before a massive retracement. Price action was trying to get back to these overextended highs but has failed in subsequent waves so watch for another potential breakdown here:

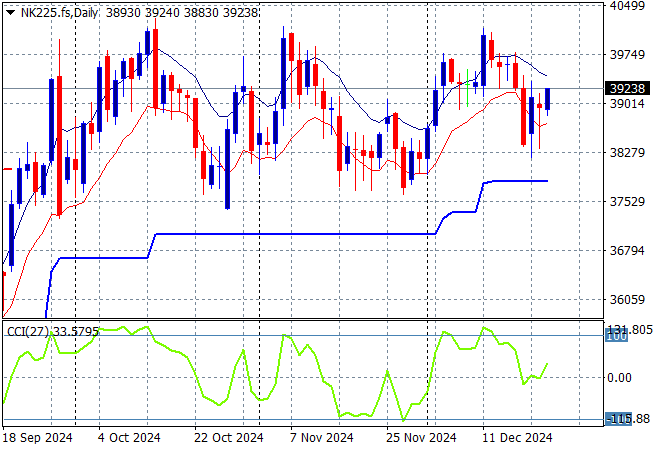

Japanese stock markets also advanced on the potential Nissan/Honda deal with the Nikkei 225 up more than 1.1% to 39161 points.

Price action had been indicating a rounding top on the daily chart with daily momentum retracing away from overbought readings with the breakout last month above the 40000 point level almost in full remission. Yen volatility remains a problem here, with a sustained return above the 38000 point level from May/June possibly on the cards as positive momentum is building:

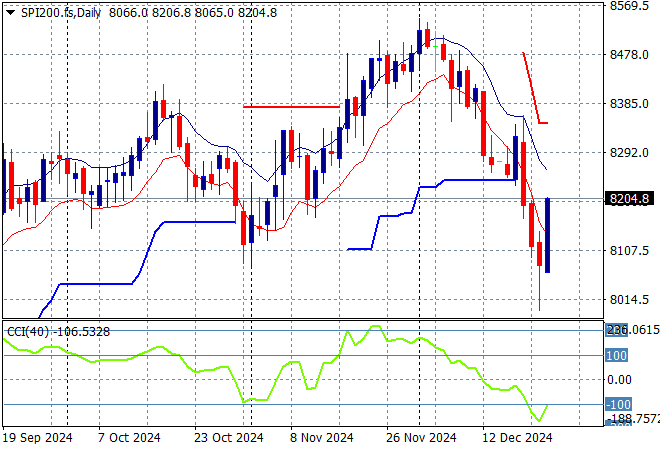

Australian stocks are finally the best performing region with the ASX200 up more than 1.6% to close at 8201 points.

SPI futures however are relatively flat despite the solid showing on Wall Street overnight. The daily chart pattern and short price action suggests this rollover has built a little too much momentum to the downside even if support at the 8400 point level was illusory indeed. Watch for a late dead cat bounce here still:

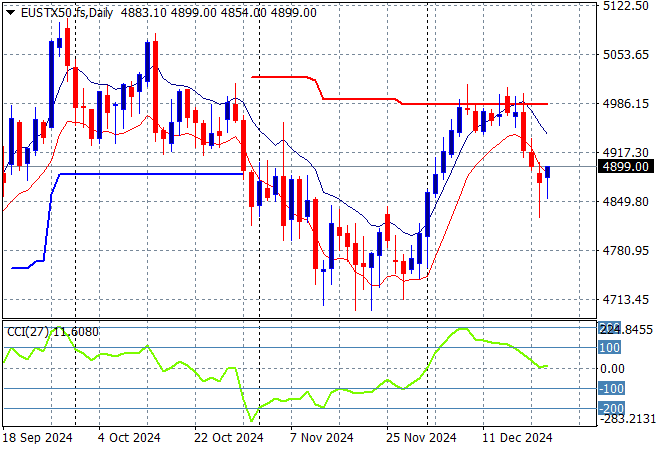

European markets are slowing down into the Xmas break with some mild pullbacks across the continent with the Eurostoxx 50 Index eventually closing 0.2% lower at 4852 points.

This was looking to turn into a larger breakout with support at the 4900 point level quite firm with resistance again unable to breach the 5000 point barrier. Price had previously cleared the 4700 local resistance level as it seeks to return to the previous highs but momentum has rolled over here with futures indicating the 4900 point level to remain steady:

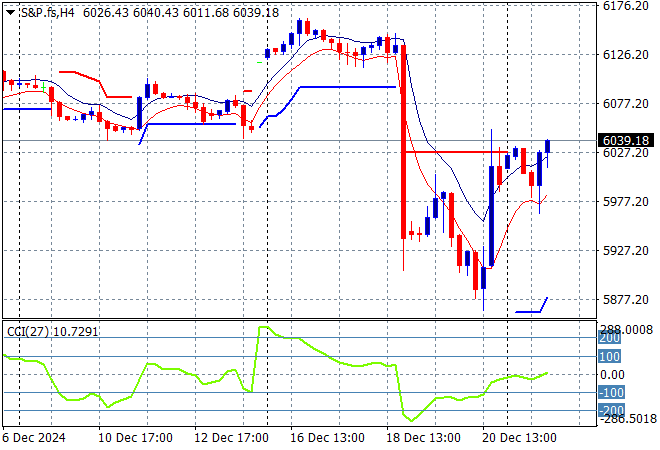

Wall Street is trying hard to get out of its recent funk on the back of the somewhat cool inflation prints with the NASDAQ up another 1% while the S&P500 pushed more than 0.7% higher to finish at 5974 points.

The Orange Santa rally is now back on track after clearing local resistance but it remains to be seen if it can fully get out of its funk through the short Xmas/NY break. As I said previously, the bottom pickers could move in swiftly given the clowns are running the circus even before opening day at the zoo so here we are:

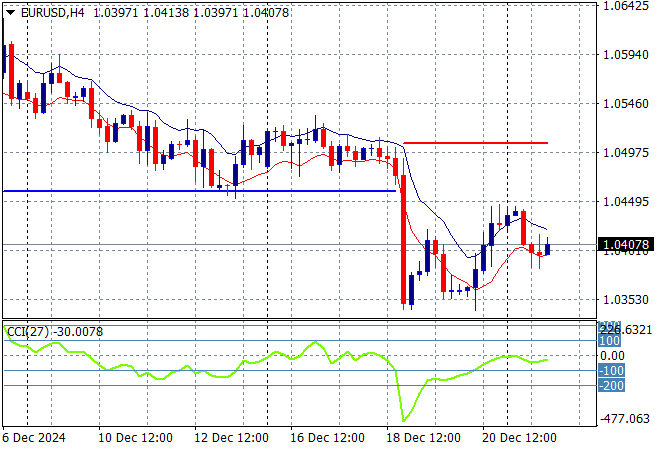

Currency markets remain in the thrall of King Dollar as the post weekend absorption of Friday night’s cooler US PCE numbers gave some oversold undollars all the reasons they needed to attempt a bounceback. However as expected this was shortlived as Euro remains well below former support with a pullback to the 1.04 handle as short term momentum is still quite negative.

This all still fits in with my contention that we are still likely on our way back to parity as traders start to price in the now very unclear future for the continent. The union currency is now making new lows and will likely slide further towards parity going into the end of the trading year:

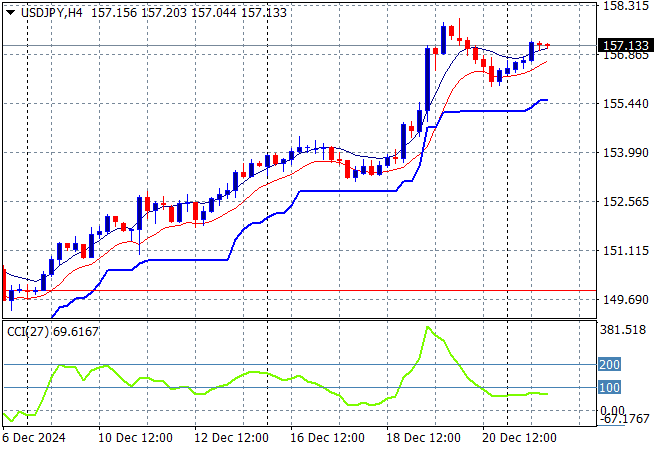

The USDJPY pair was able to push a little bit higher following its Friday pullback, getting just above the 157 handle overnight in a relatively strong move overall.

Short term momentum has reverted out of extremely overbought settings but is still very positive indeed as price action settles down but there is still potential for more upside here dependent on trading activity this Xmas week:

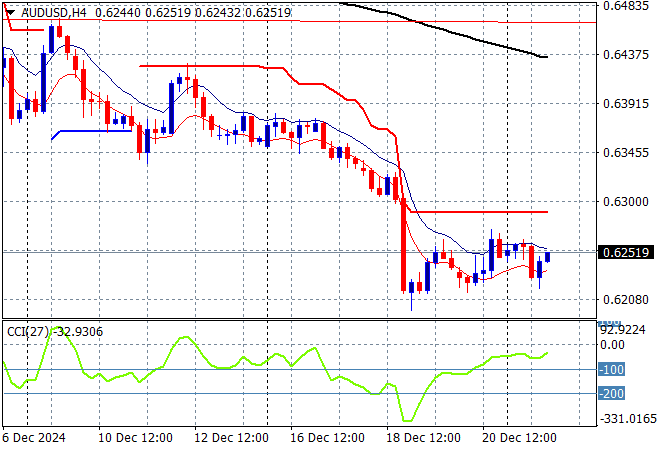

The Australian dollar remains one of the most depressed undollars as the RBA plays fiddlesticks amid macro volatility and local recessions with the very weak fightback on Friday night turning into nothing sustainable as it still can’t get any traction above the 62 handle.

This breakdown has been on the cards for weeks and will reverberate into the new year as the currency finally reweights according to its position in the global economy – lower tier. Watch for overhead ATR resistance on the four hourly chart to be rejected again:

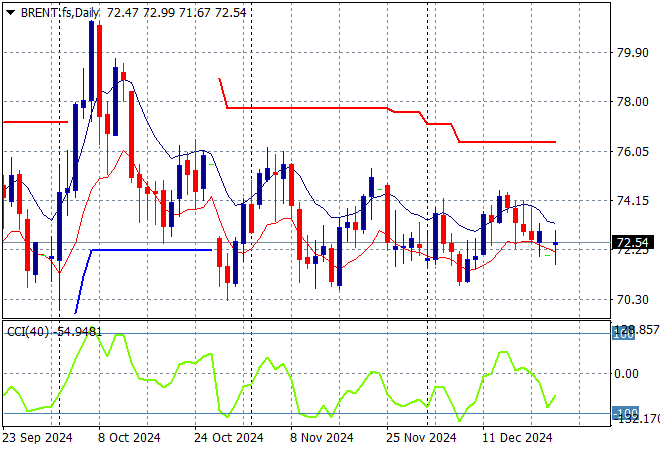

Oil markets are trying to re-engage post the OPEC meeting as Brent crude tries to get out of its depressed mood around the $72-73USD per barrel level, but was again held well below the $73 level overnight as it still can’t manage to fulfill this bounce.

The daily chart pattern continues to tighten like a spring with short term momentum definitively in negative territory as medium term price action still supports a downtrend with my contention of another sharp retracement forthcoming if the $70-72 zone is not defended:

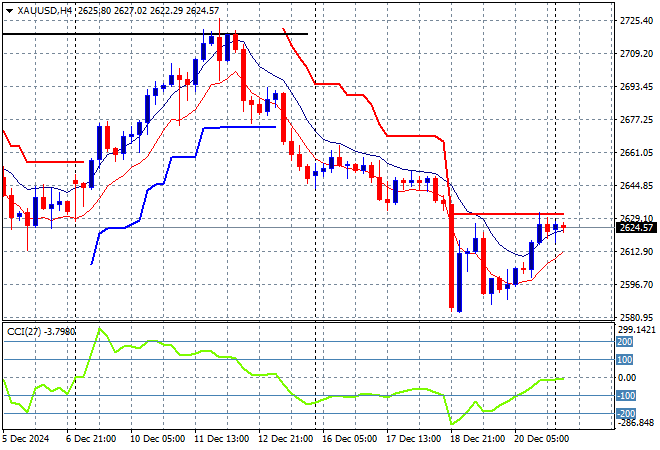

Gold suffered almost as much as the Australian dollar on the Fed cut/hold but tried to sustain a return above the $2600USD per ounce level on Friday night with little success, steadying overnight just below local resistance at the $2630 level.

Price action had been accelerating in confidence in early December as new levels of support were being created regardless of USD strength but this pullback and rebound both had been fighting too much under the $2700 zone so I have been skeptical of any upside potential. And here we are with a new low for that is threatening the year long uptrend:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out/wrong on your position, so cry uncle and get out!