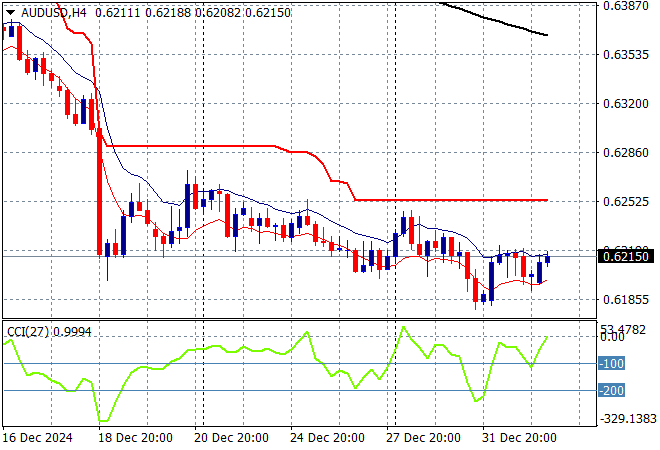

China is again in the forefront of news in the last trading session of the first week of the trading year with speculation of an imminent rate cut by the PBOC plus more “support” from state planner. Aka turning Japanese. The USD remains firm against the undollars with Euro treading water above the 1.02 handle while the Australian dollar is getting no traction as it barely holds on to the 62 cent level.

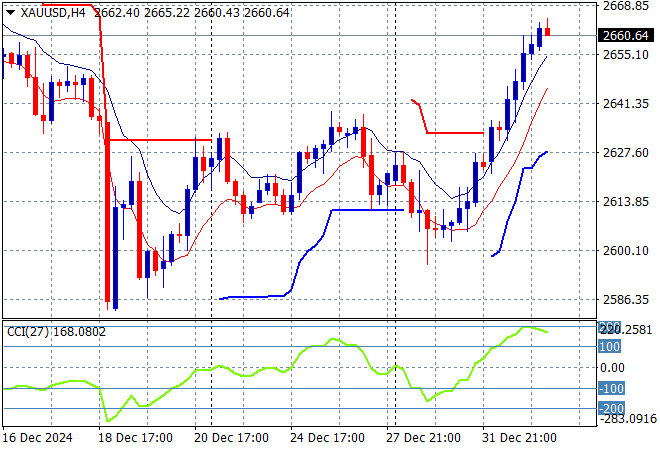

Oil futures are up slightly again with Brent crude lifting through the $76USD per barrel level while gold is slightly rolling over after its break out above local resistance at the $2630USD per ounce level:

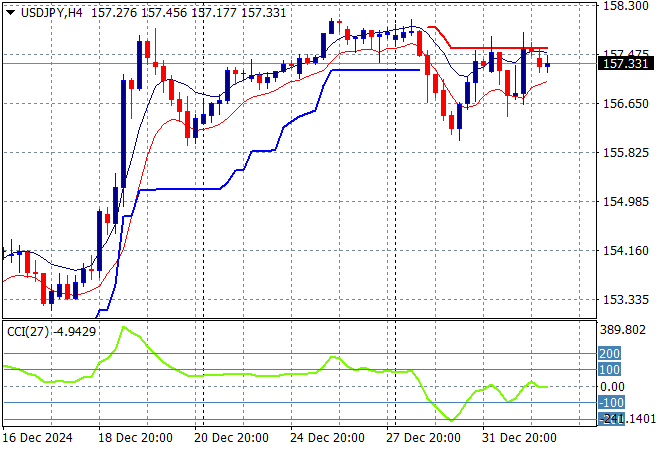

Mainland Chinese share markets are still looking weak as they slide lower into the afternoon session with the Shanghai Composite down more than 0.8% to remain well below the 3300 point level while the Hang Seng Index has rebounded by 0.5% to 19726 points. Japanese stock markets remain closed while the USDPY pair has pulled back slightly to just above the 157 level:

Australian stocks are again the best performing in the region with the ASX200 up more than 0.6% to close at 8250 points while the Australian dollar has held above the 62 handle after making a new yearly low just after Xmas, but this looks ominous to say the least:

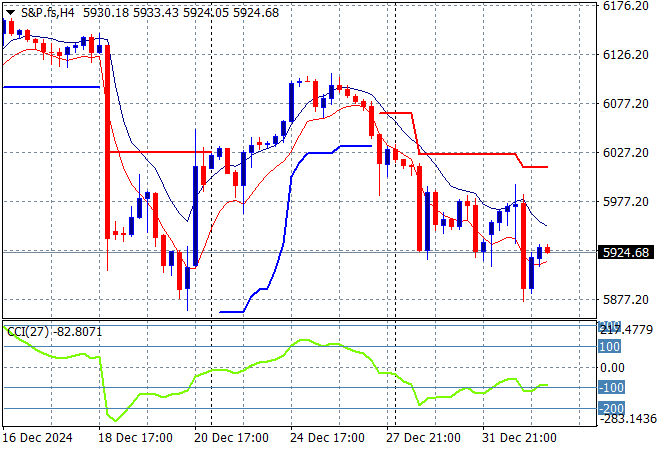

S&P and Eurostoxx futures are trying to lift higher from their recent steep losses as we head into the London session with the S&P500 four hourly chart showing momentum barely out of its oversold condition as it fails to tackle short term resistance levels:

The economic calendar ramps up with German unemployment and the latest US ISM Manufacturing Survey.