Wall Street had another tipsy session overnight as the latest US initial jobless claims came in slightly lower than expected with the Trump tariff shotgun approach still weighing on risk markets, let alone the bluster about invading Canada and Greenland. Bond markets settled down somewhat but remain volatile while the USD continues to come back to strength against most of the undollars. The Australian dollar remains depressed as markets expect the RBA to cut rates before the next Federal election in May as a result of yesterday’s softer than expected monthly CPI print.

US Treasury yields were flat this time with the 10 year still hovering below the 4.7% level while oil markets are pulling back slightly as Brent crude closed below the $77USD per barrel level to extend its new weekly high. Gold however inched higher to get return to its previous high around the $2660USD per ounce level.

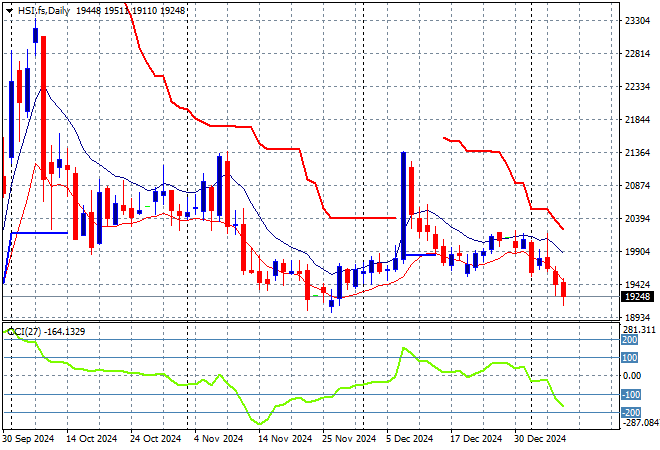

Looking at stock markets from Asia in yesterday’s session, where mainland Chinese share markets rolled over sharply in afternoon trade with the Shanghai Composite down more than 1.5% before being able to recover to get back above the 3200 point level while the Hang Seng Index was unable to fill in the gap to close some 0.9% lower at 19279 points.

The Hang Seng Index daily chart shows how resistance formed around the 21000 point level with only one false breakout in late November squashed back to the 20000 point level where price action has stayed since. This is still setting up for another potential breakdown here:

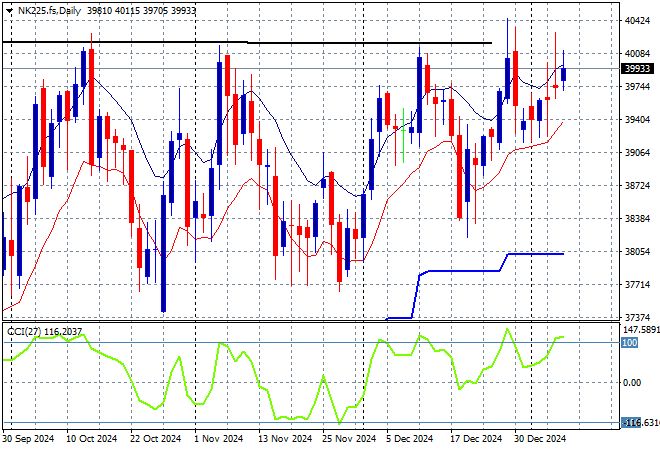

Japanese stock markets were off slightly with the Nikkei 225 unable to hold above 40000 points, closing 0.3% lower at 39981 points.

Price action had been indicating a rounding top on the daily chart with daily momentum retracing away from overbought readings with the breakout last month above the 40000 point level almost in full remission. Yen volatility remains a problem here, with a sustained return above the 38000 point level from May/June possibly on the cards but resistance is firming:

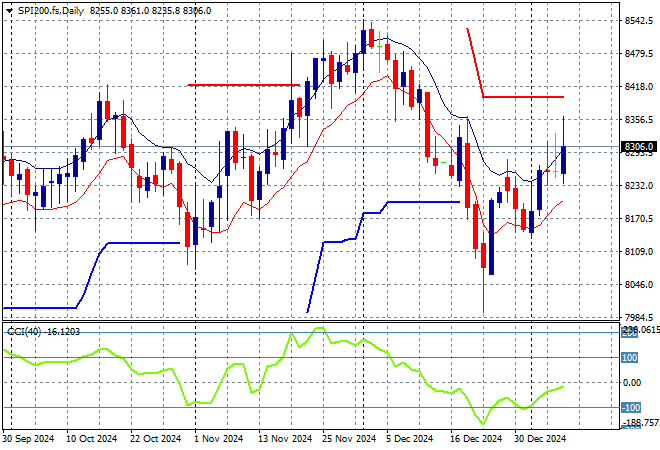

Australian stocks were the best performing in the region due to the monthly inflation print and RBA rate cut scuttlebutt with the ASX200 closing nearly 0.8% higher at 8349 points.

SPI futures are off by 0.4% or so given the uneasiness on Wall Street overnight. The daily chart pattern and short price action suggests this rollover has built a little too much momentum to the downside even if support at the 8400 point level was illusory indeed. The dead cat bounce doesn’t look like its going to repeat here on AUD weakness and rate cuts however:

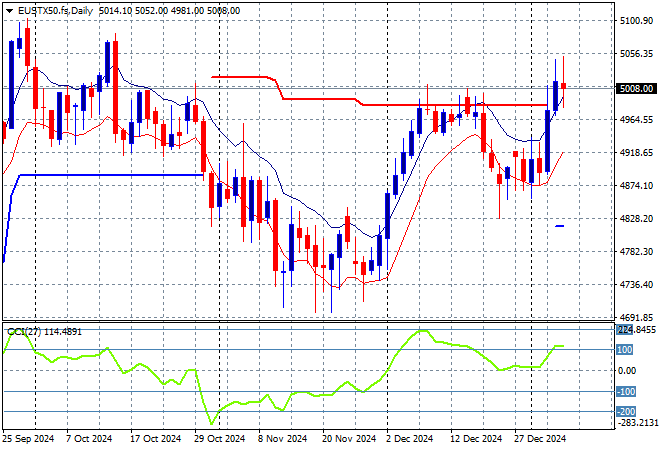

European markets failed to build overnight on more Trumpiness with the Eurostoxx 50 Index closing 0.3% lower to pullback slightly below 5000 points.

This was looking to turn into a larger breakout with support at the 4900 point level quite firm with resistance unable to breach the 5000 point barrier in recent months. Price had previously cleared the 4700 local resistance level as it seeks to return to the previous highs but momentum has pick up strongly here with the 4900 point level turning into strong support:

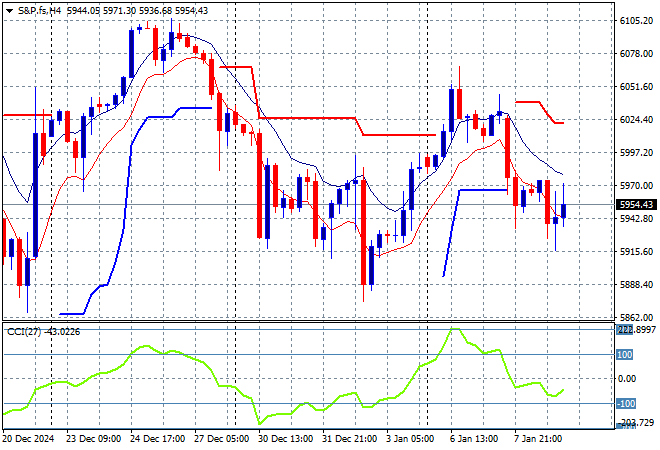

Wall Street also can’t gain traction with the initial jobless claims messing up confidence with NASDAQ slipping slightly while the S&P500 barely put on any runs, closing at 5918 points.

Short term price action looks somewhat ominous but never discount the bottom pickers to get this back on track with a potential rebound off the 5900 point support zone if it gets back down there again:

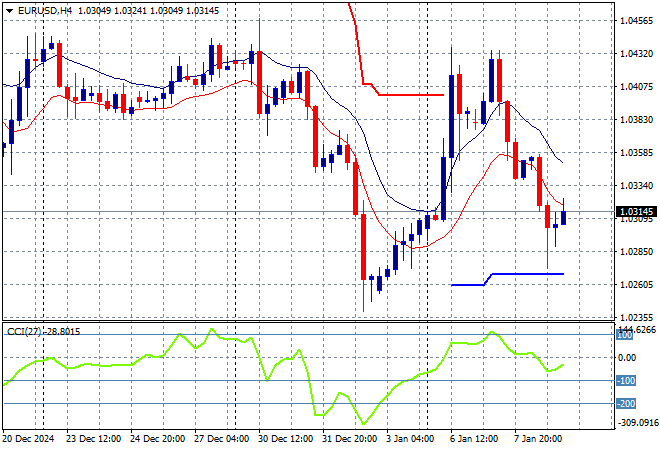

Currency markets remain in the thrall of King Dollar with the latest US initial jobless claims and FOMC minutes coupled with broader macro concerns, read: Trump Circus caused a run again. Euro fell back to the 1.03 handle, wiping out its recent post NY progress.

The union currency is now making new lows and will likely slide further back towards the new year low at the 1.02 level first:

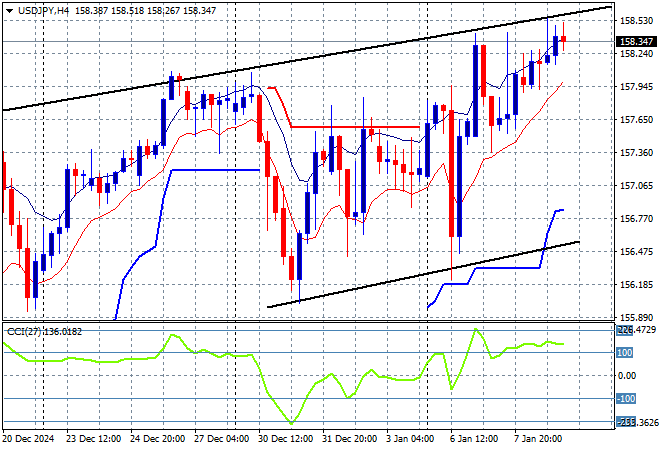

The USDJPY pair was able to move slightly higher as it remains very well supported in the short term, pushing further above the 158 handle overnight.

Short term momentum has reverted out of extremely overbought settings but is still very positive indeed as price action settles down but there is still potential for more upside here dependent on trading activity as the new year begins.

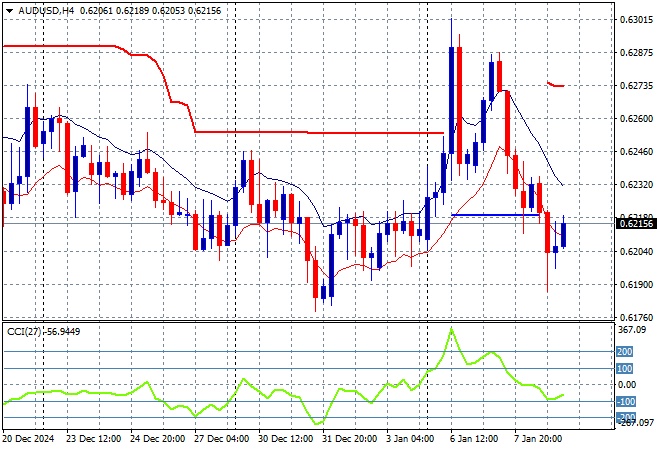

The Australian dollar remains one of the most depressed undollars with the very weak fightback before Xmas turning into nothing sustainable as it loses traction and retreats in full back down to the 62 handle in the wake of yesterday’s monthly CPI print..

This breakdown has been on the cards for weeks and will reverberate into the new year as the currency finally reweights according to its position in the global economy – lower tier. Watch for overhead ATR resistance on the four hourly chart to be rejected again:

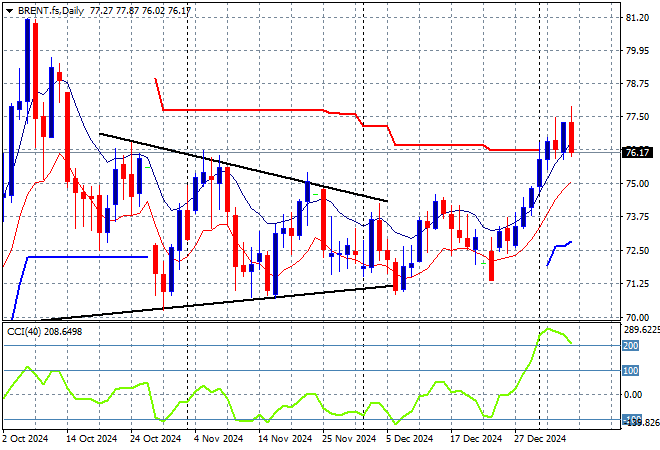

Oil markets are doing well to re-engage post the OPEC meeting as Brent crude got out of its depressed mood around the $72-73USD per barrel level recently, but this push above the $77 level has seen a mild pullback after what looked like a solid breakthrough.

The daily chart pattern has broken out of its spring formation with short term momentum bursting into overbought territory with a run up to the $80 level probable, but needs another breather first:

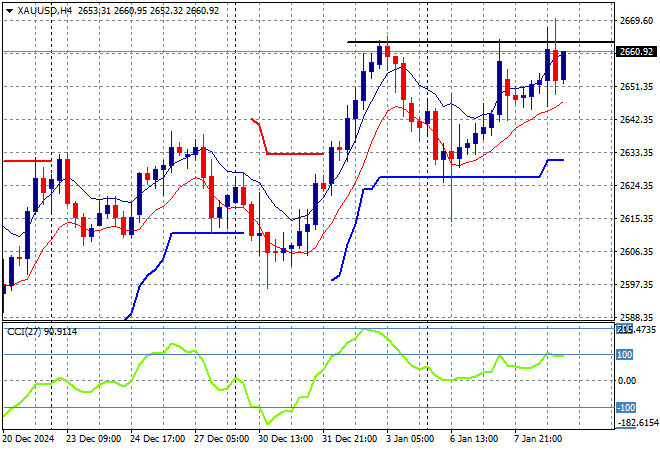

Gold is trying to get back on track and was able to advance further overnight, matching its previous recent high at the $2660USD per ounce level, filling the mild retracement from last Friday night.

Price action had been accelerating in confidence in early December as new levels of support were being created regardless of USD strength but this pullback and rebound both had been fighting too much under the $2700 zone so I have been skeptical of any upside potential. However this does look interesting if it can break through:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out/wrong on your position, so cry uncle and get out!