Donald Trump’s assault on the US federal government and the world’s interlinked manufacturing system have together reached an economic tipping point.

“It seems almost unavoidable that we are headed for a deep, deep recession,” said Jesse Rothstein, Berkeley professor and former chief economist at the US Labour Department.

…“I think we’re going to see historically large drops,” Rothstein said. “Losses of 400,000 a month are not implausible because people are getting nervous out there.

Advertisement

“It is not just the federal employees being fired: it’s all the other people worried they could be next, so they are cutting back too.”

Fiscal consolidation is fine as far as it goes. But this looks more like a wildly flailing fiscal chainsaw. DOGE is incoherent, slashing and burning everything in its wake at lightning speed.

Advertisement

Then there is the “woke clearout,” which is far bigger than it appears. AEP again.

You only have to read the details of Executive Order 14154 to see there will be real economic consequences. Section 7, Terminating the Green New Deal, reads: “All agencies shall immediately pause the disbursement of funds appropriated through the Inflation Reduction Act or the Infrastructure Investment and Jobs Act”.

Judges have intervened, but almost $US300 billion ($473 billion) left from the Infrastructure Act remains in limbo. Freyr Battery has cancelled a $US2.6 billion plant in Georgia linked to the IRA. Kore Power has dropped its $US1.2 billion energy storage project in Arizona. Heliene has shelved a $US200 million solar-cell facility. Nel has halted its $US200 million gigafactory in Detroit. Prysmian will not be making undersea cables for offshore wind after all.

The US economy has been displaying late-cycle fatigue for some time, which is no doubt why Warren Buffett more than doubled his holding of cash and treasury bills to $US334 billion last year. We can only guess at his real reasons for battening down the hatches: perhaps he fears the delayed effects of past Fed tightening, or perhaps he dislikes anarchy.

Advertisement

Anarchy is the word. Trying to fathom what is coming next from the child president’s mouth is a fool’s errand.

These outbursts become proclamations and laws or are revoked moments later or buried in courts interminably.

In short, as AEP says, the danger of overshooting job cuts is greatly exacerbated if it mushrooms into a stall in investment.

Is there a plan behind the madness? Charlie McElligott at Nomura thinks so.

Advertisement

We can probably all agree that this “plan” is sensible enough. It is the execution of it that worries me.

Advertisement

It appears bastardised by Trump’s grabbag of lunatics.

I can’t tell if Trump’s method of government, like Hitler’s, is to have various lieutenants at each other’s throats, or if it is the lieutenants that have control of him with a quick kiss on the ring to free themselves to deploy whatever ideological agenda takes their fancy under the rough rubric of MAGA.

Whether it is Musk and DOGE, Lutnick and climate change, Hegseth and trans-military, the chopping does not appear to have an obvious real-world limit other than a collapse in either service delivery or the economy.

The danger of overshooting is very high amid this anarchistic governance.

Michael Hartnett at BofA does not mince words on the outcome.

Tale of the Tape: on election day S&P500 closed at 5783; we say this is first strike price of Trump put, below which “Stocks Down Under Trump” headlines begin, below which investors currently long risk would very much expect and need some verbal support for markets from policymakers.

The Biggest Picture: we say most important price to watch= IJR (US smallcap ETF); no breakout above its ‘21 highs ($120–Chart 2) with MAGAbackdrop of tariffs, FDI inflows, tax cuts, deregulation, Fed cuts…tells you bonds outperform stocks.

Advertisement

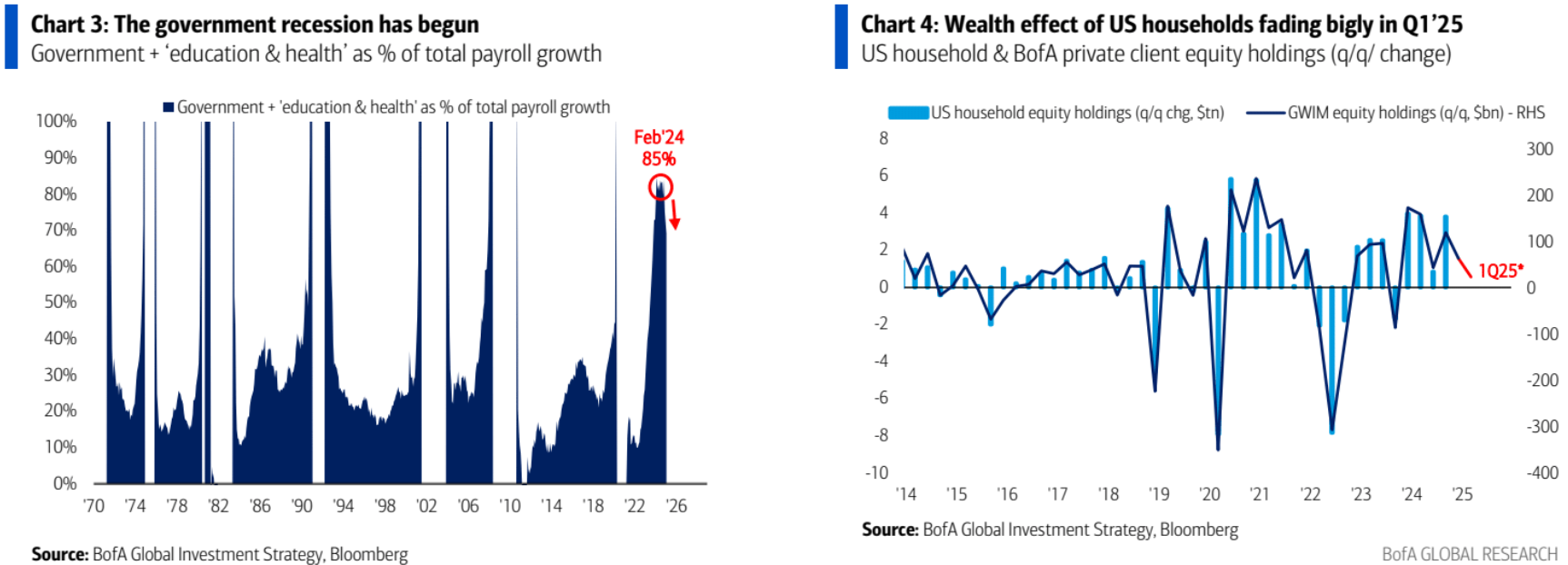

We said: buy US long bonds…a. Trump won’t go big tariffs as political malpractice to allow 2nd wave of inflation, b. DOGE = $7tn US Government set to contract and “G” (up 65% past 5 years) has been huge driver of nominal GDP growth (up 50% over same period), c. DOGE = weak payrolls (government + quasi-govt education/health currently accounting for 70% of US payroll growth (was 85% a year ago–Chart3),d. DOGE = higher US savings rate for “poor” as conviction in “fiscal bailouts” ends, and wealth effect for “rich” fading quickly (we calculate via BofA private client equity holdings that US household equity wealth on course for $0.6tn gain in Q1 vs $3.8tn in 3Q’24 & $1.6tn in 4Q’24–Chart4).

You said: yeah, and long bond decent hedge against S&P500, but we need a recession to own bonds, Trump policies likely reverse before recession, and tax cuts in H2 mean deficit will get worse.

Advertisement

There are already unsettling signals emanating from the US economy.

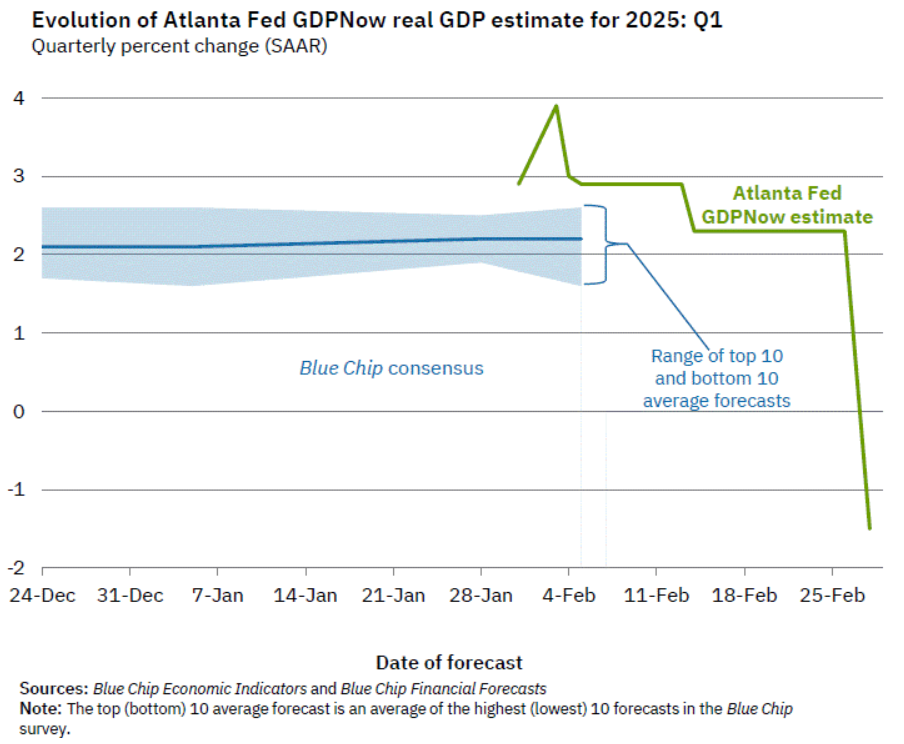

The Atlanta Fed GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2025 is -1.5 percent on February 28, down from 2.3 percent on February 19. After recent releases from the US Bureau of Economic Analysis and the US Census Bureau, the nowcast of the contribution of net exports to first-quarter real GDP growth fell from -0.41 percentage points to -3.70 percentage points while the nowcast of first-quarter real personal consumption expenditures growth fell from 2.3 percent to 1.3 percent.

GDPNow is volatile and has been heavily influenced by trade data suggesting tariff frontrunning, still…

The Flash Services PMI crashed into contraction, and any bounce in manufacturing is also probably tariff frontloading.

PCE was weak.

It could be argued that all of these were fire and weather-affected, so it is not as bad as it seems. The Market Ear.

So much uncertainty

Trade policy uncertainty has spiked higher.

Source: Deutsche

Advertisement

Tariffs will lift US structural inflation

Tariffs will lift US structural inflation expectations from an already elevated level.

Source: BCA

Who let the DOGE out?

Recent events have shifted risks in the direction of a larger fiscal drag than research assumes. Whether spending cuts materialize from DOGE or the budget process, they are likely to come in categories with high multipliers. On employment, don’t forget about the freeze in federal hires…

Advertisement

Source: Morgan Stanley

The government recession has begun

Government + ‘education & health’ as % of total payroll growth.

Source: BofA

Advertisement

Doubting Trump and ‘US exceptionalism’?

Trump rally fades again as policy plans become clear – tariffs were not priced in by markets.

Source: Macrobond

Starting to worry about growth?

Markets are pricing significantly lower Fed rates in 2026.

Source: Macrobond

Advertisement

US growth rolling over as Trump stimulus fails to materialize?

Unsustainable demand bump? Consumers have turned more negative since inauguration.

Source: Macrobond

Goldman “gives up”…

“We trim our 2025 EPS growth forecast from 11% to 9% and maintain our 2026 forecast of 7%. Our revision reflects the fact that EPS growth in 2024 was stronger than expected but economic data in 2025 have been softer than expected…..economic data in 2025 have been slightly weaker and the tariff outlook slightly more hawkish than we expected.”

Consensus catching-down

Consensus 2025 EPS growth estimates have come down recently.

Source: FactSet

Advertisement

Uptick

Probability of a recession in the US, UK, and Europe starting to move higher.

Source: Apollo

Markets trading it

Cyclicals have sharply underperformed Defensives in recent weeks.

Source: Goldman

Advertisement

The Trump recession?

“Not so fast”, says Steven Blitz.

“Weaker—but not weak—consumer confidence numbers reflect worsening inflation expectations rather than weaker growth. After a strong Q4, data have softened, especially sentiment, giving overextended markets an opportunity to correct. Market participants are overlooking factors like bad weather, worsening wildfires, and the lagging impact of the Fed waiting too long to cut financing costs. Instead, they’re focusing on deportations, tariffs, program cuts, and fewer government employees to conclude what some economists have long argued—without federal spending, the economy is headed downward. Our “secret sauce” for growth in 2025 has always been accelerated private capital spending, fueled by Trump’s influence in spirit and deed, rather than suppressed by his actions.”

Credit spreads have barely budged, supporting the notion that everything is fundamentally OK.

But, there is extreme uncertainty in the air, and if credit does fray, then the spooking will mushroom.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.