Last week, the Reserve Bank of Australia (RBA) released Q4 2024 data on household debt.

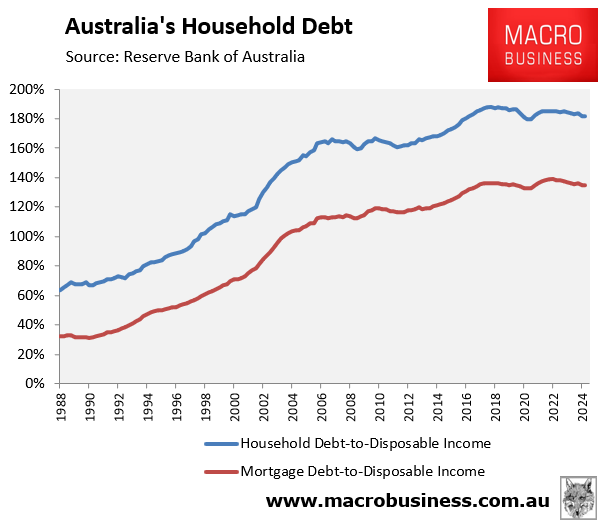

As illustrated in the chart below, the ratio of household debt to income was 182% in Q4 2024, tracking close to a record high. This was driven by mortgage debt, which was tracking at 135% of household disposable in Q4.

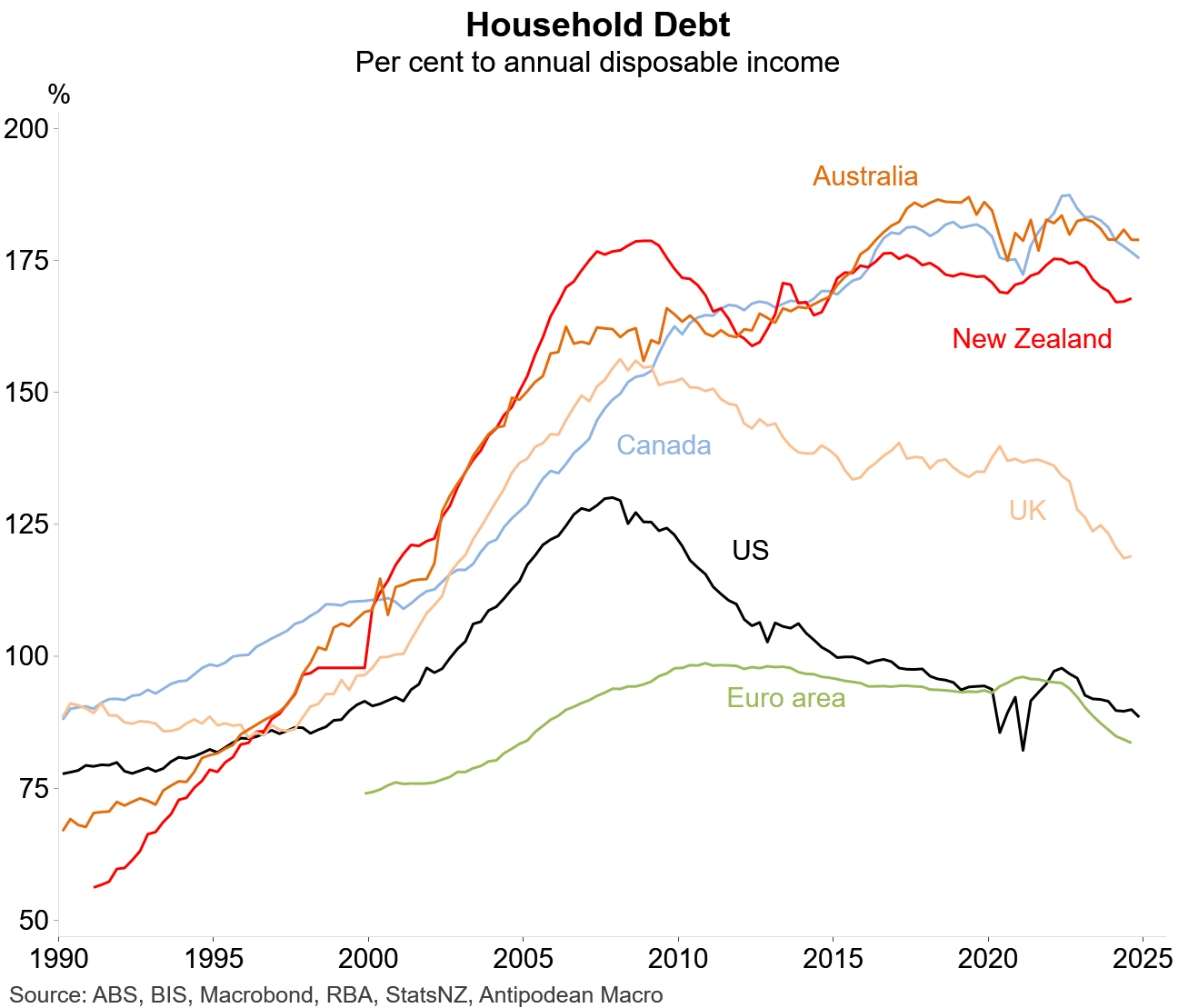

The following chart, courtesy of Justin Fabo from Antipodean Macro, illustrates that Australia’s household debt remains among the highest in the world, surpassing that of Canada, New Zealand, the United Kingdom, the United States, and the European region.

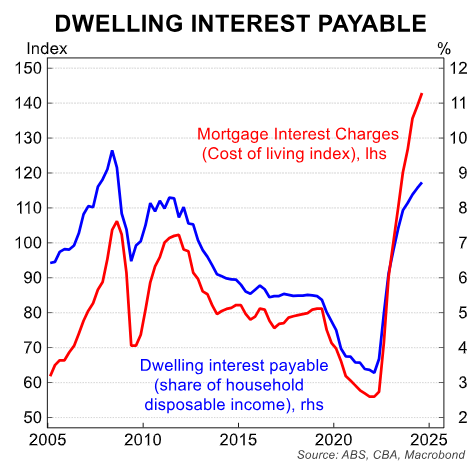

CBA also shows that dwelling interest payable as a share of household income was tracking close to a record high, just below the peak of the Global Financial Crisis.

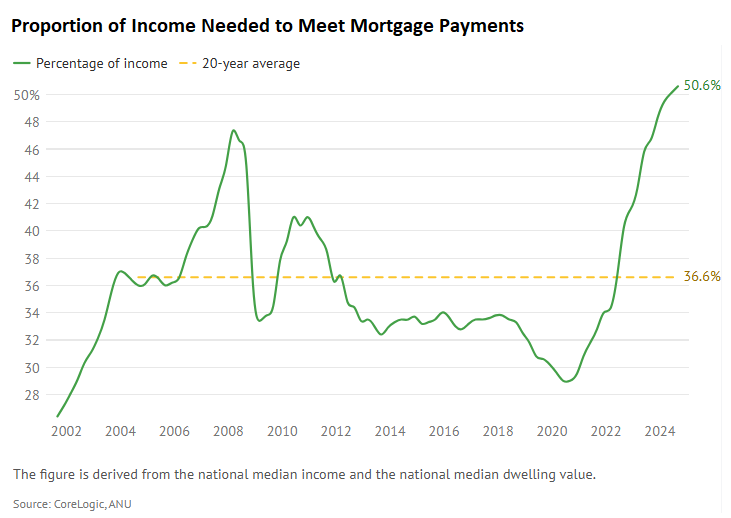

Finally, the following chart from Domain, compiled from CoreLogic data, shows that the share of income required to meet mortgage repayments on the median-priced home reached a record high of 50.6% at the end of 2024.

The above data is for Q4 2024 and, as such, predates the RBA’s 0.25% interest rate reduction in February. This rate cut would have lowered interest payments and improved affordability.

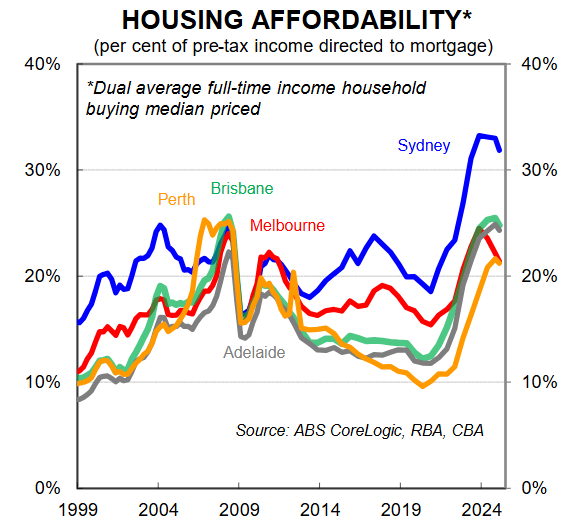

Indeed, the following chart from CBA shows that housing affordability, based on a 20% deposit for dual average full-time income earners buying a median-priced home, has eased in most capital cities.

CBA attributes this improvement in affordability to the 0.25% RBA rate cut and softer home prices, which has improved affordability in Sydney and Melbourne in particular.

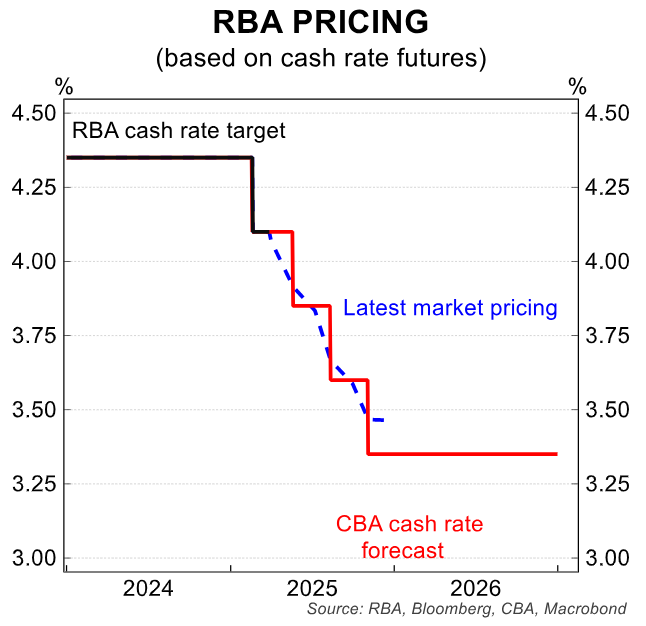

Most economists expect the RBA to cut interest rates another three times this year.

As a result, mortgage affordability is expected to continue improving.