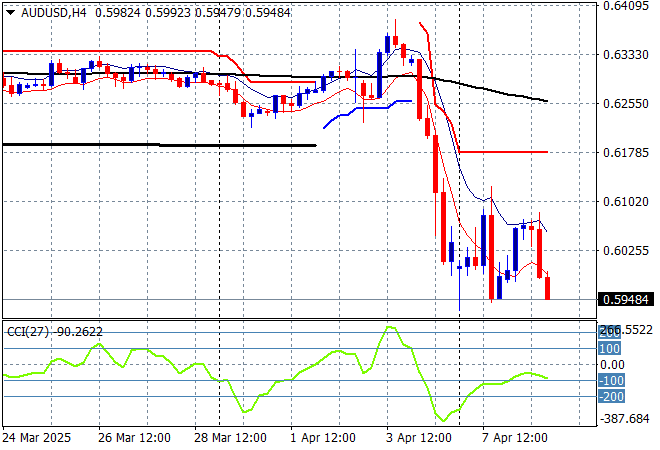

Another ugly night on Wall Street that started out as a lovely time had by all as equity markets across both sides of the Atlantic rebounded on hope that everything is going to be ok. But that was a lie as the Fanta Fuhrer again spoilt the party after first suggesting a delay in new tariffs on China before their silence thereafter saw Yuan weaken to new record lows with other currencies falling in time. Bond markets caused more wreckage particularly on the long end of Treasuries while Wall Street gave up a 4% rally to fall 2% or more as realisation set in that yes, the kindergarten economists remain in charge. The Australian dollar fell back to a new low at the mid 59 cent level against USD.

10 year Treasury yields surged again with another push above the 4.2% level with worrying signs on the long end of the curve as well as huge deficits seem baked in here while oil prices made new lows, with Brent crude now down to the $61USD per barrel level. Gold also suffered further falls and remains well below the $3000USD per ounce level, currently at the $2950 area.

Asian equity futures don’t look too happy with a variety of different breeds of dead cat’s bouncing all over the place, ready to roll over….

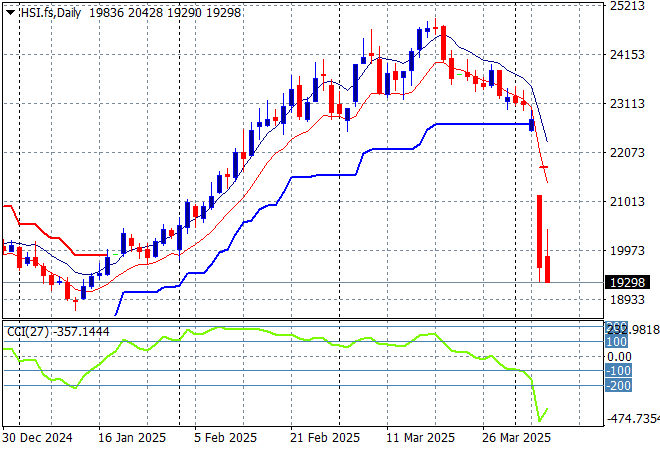

Looking at stock markets from Asia from yesterday’s session, where mainland and offshore Chinese share markets were able to tread water in a calm but frantic way, watching what will happen with the next spat of tariff/counter-tariff moves with the Shanghai Composite eventually closing up more than 1% to get above the 3100 point level while the Hang Seng Index has moved slightly higher, closing up 1.5% to 20126 points.

The Hang Seng Index daily chart shows how this recent move looked unsustainable to the upside after recently setting up for another potential breakdown around the 20000 point level. Momentum has reversed completely to panic selling with support at the 22000 point level completely wiped out. More to come?

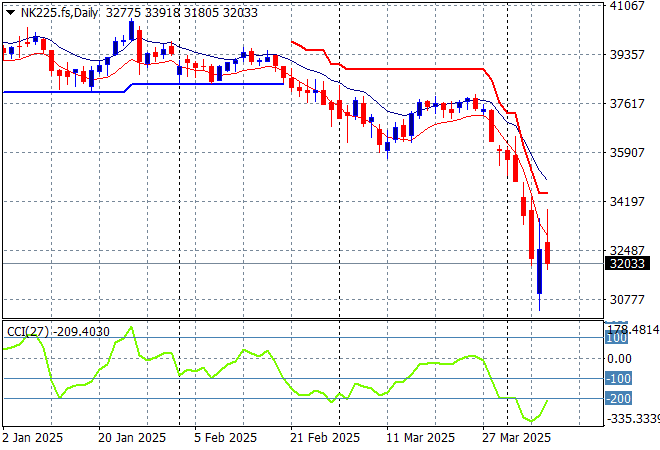

Japanese stock markets were very positive however and have soared higher with the Nikkei 225 up 6% to 32908 points.

Price action had been indicating a rounding top on the daily chart for sometime now with daily momentum retracing away from overbought readings with the breakout last month above the 40000 point level now in full remission. Yen volatility alongside correlation with other risk markets are the main problem here, with futures are indicating a pullback on the open this morning:

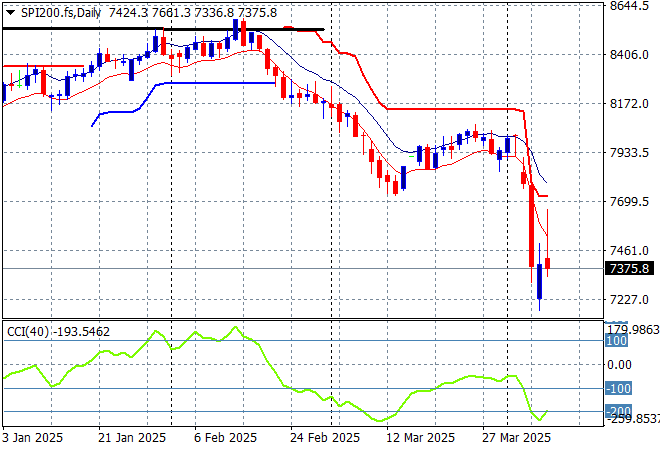

Australian stocks had a modest bounce back with the ASX200 closing some 2% higher at 7510 points.

SPI futures are down another 2% so yesterday’s return will be wiped out probably in today’s session given the huge reversal of fortune on Wall Street from overnight. The daily chart pattern however suggests further downside is inevitable as the Chinese counter-counter tariffs take effect and the Australian dollar continues to crash:

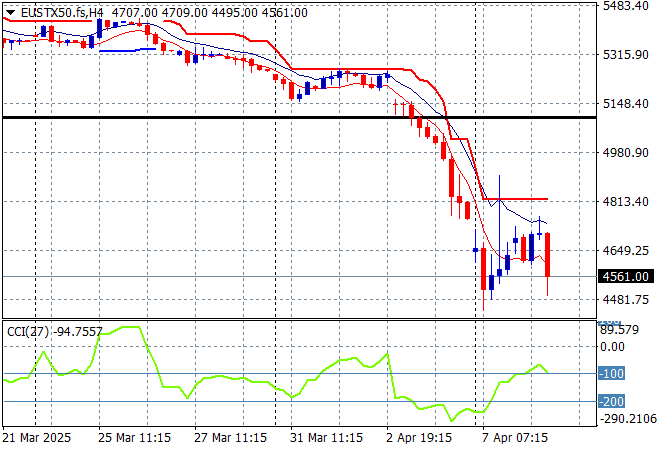

European markets were finally able to escape the widespread selling with some short covering moves across the continent with the Eurostoxx 50 Index finishing up 2% to 4773 points.

Support at the previous monthly support levels (black line) at 5100 points failed to hold so 2024 lows at the 4400 point level are now in sight, baring a dead cat bounce here. Good time for more European defence stock purchases perhaps, although futures are again rolling over for another dead cat:

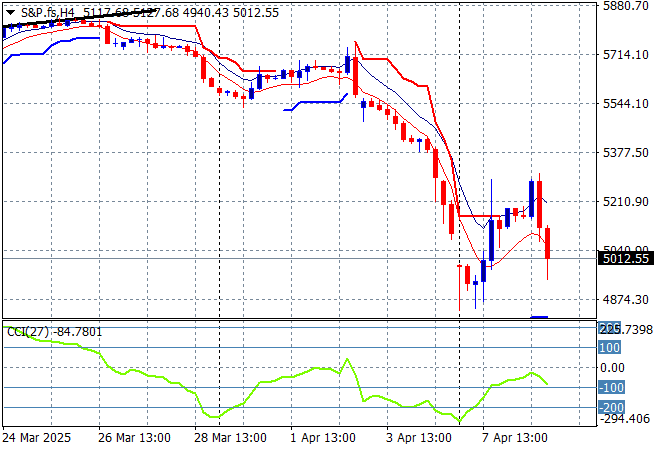

Wall Street was epically volatile due to of course an epically stupid White House with the NASDAQ actually up 7% at one stage before giving that all up to fall 2% while the S&P500 lost 1.5% to eventually fall below the 5000 point level.

The Trump pump and dump scheme is definitely in dead cat bounce phase here as false hope builds that some relief is around the corner. Its not – this could go much lower with the former lows at the 5000 point level the area to watch:

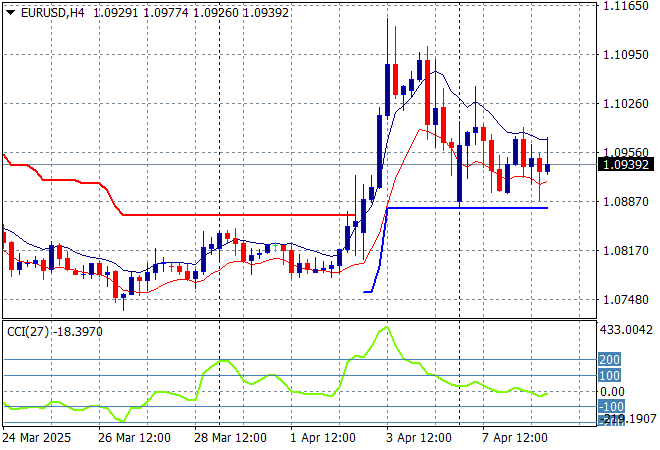

Currency markets are swinging back to “King” Dollar amid the volatility as China and other nations retaliate with Euro slowly continuing its reversion back down to the 1.09 level with Pound Sterling remaining at a four week low.

The union currency spiked up through the 1.11 handle before retracing in the previous session but couldn’t find support at the 1.10 level after the monthly US employment print on Friday and is now getting pushed back towards the 1.09 level proper where a new battle will be fought:

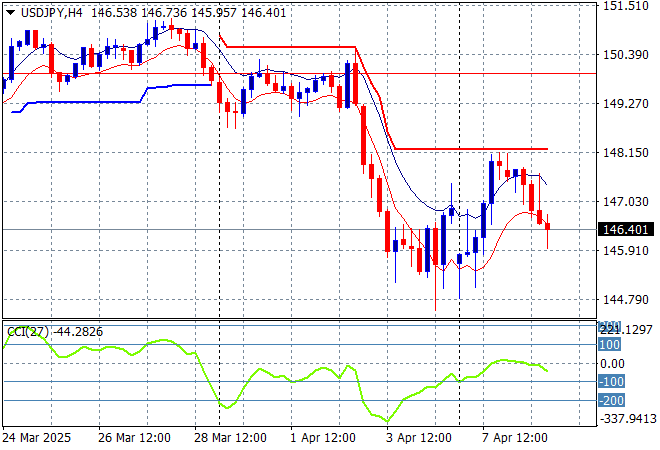

The USDJPY pair bounced back after its sharp decline, but has again rolled over in late trade after hitting short term resistance overhead at the 147 level.

Short term momentum was extremely oversold and showed a potential swing play here as everyone scratches their head to work out what’s going on with Japanese export industry likely to crumble unless some significant moves are made by the BOJ and Japanese government alongside China:

The Australian dollar continues to have a wild ride like other undollars but due to facing far more headwinds from commodity worries it fell to the mid 59 cent level overnight, making a new low in the process.

Stepping back for a longer point of view (and looking at the trusty AUDNZD weekly cross) price action is now solidly below the 200 day MA (moving black line) and a new five year low – yes we are back to COVID times. Watch out below:

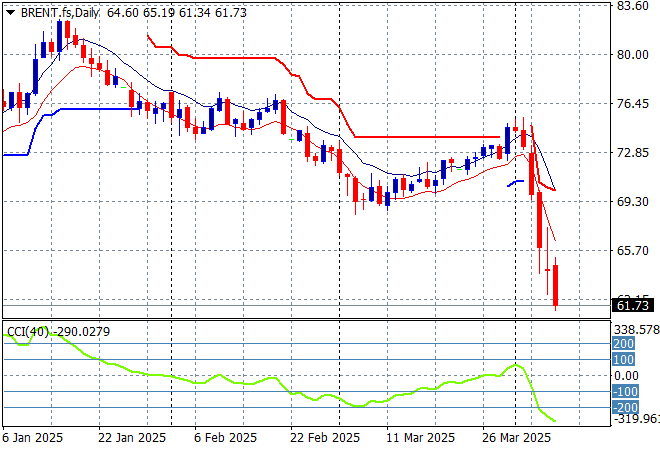

Oil market are seeing the sharp reversal continue with Brent crude pushed below the $62USD per barrel level overnight for a new low

The daily chart pattern shows the post New Year rally that got a little out of hand and now reverting back to the sideways lower action for the latter half of 2024. The potential for a return to the 2024 lows was building here before this short term bounce and is now baked in and then some as demand will collapse:

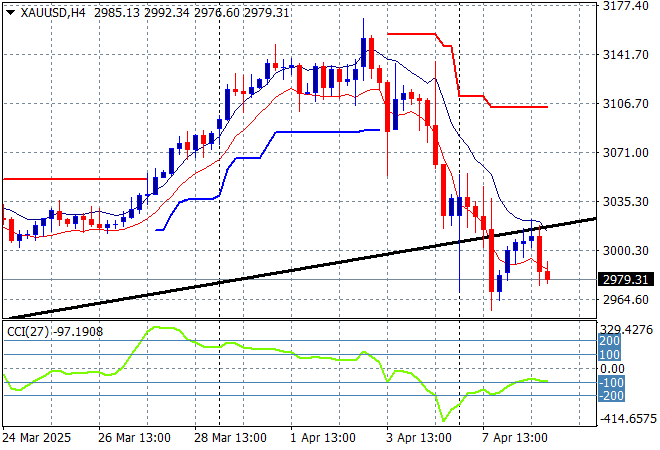

Gold suffered further volatility which could be its correlation with silver, but also a large return to USD flows as the shiny metal remained below the $3000USD per ounce level after recently breaching its long term trendline.

Short term support hasn’t held here with the potential to springboard from here on USD weakness starting to falter as the main trendline is broken so watch for a return to below the $2950 level next:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out/wrong on your position, so cry uncle and get out!