Progressive think tank Per Capita has released a report criticising the low wage growth experienced by young Australians, which has prevented them from purchasing a home.

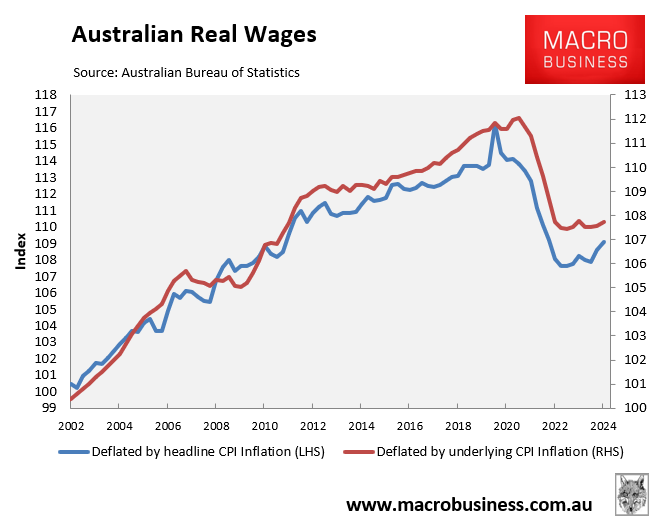

Per capita claims young Australians have suffered from a “lost decade during which real wages barely grew”.

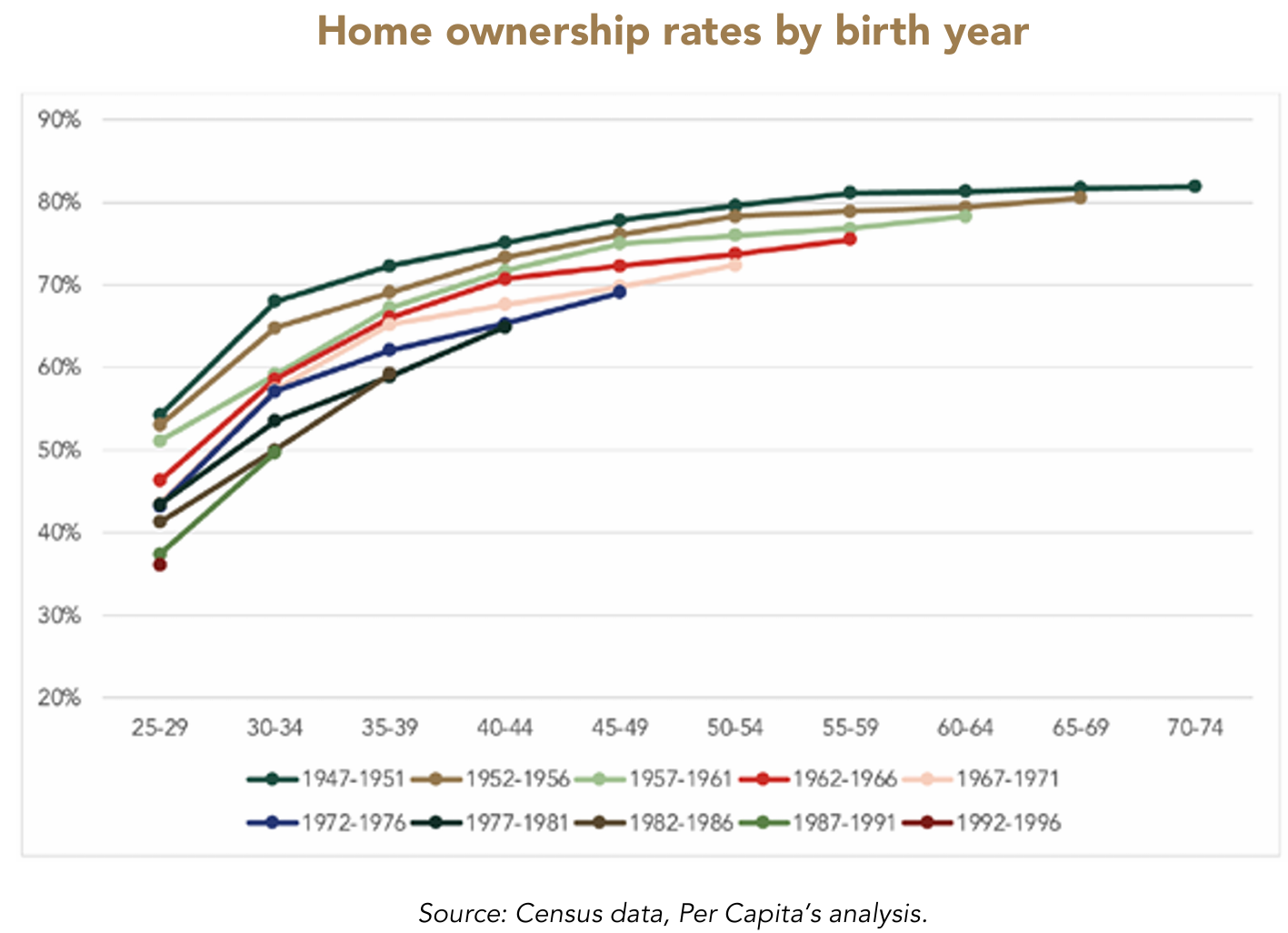

At the same time, home ownership rates for younger Australians collapsed.

“In 1971, Census data showed that 64% of people aged between 30 and 34 owned or were buying their home; by the 2021 Census, this had fallen to just 50%. Similarly, while 50% of those aged 25 to 29 were homeowners in 1971, fifty years later just 36% of people in their late twenties were buying a home”.

Per Capita argues that stagnant real wages are a major barrier to homeownership.

“While wages kept pace with home prices it was possible to save a deposit on a first home within three to five years, and this required prospective buyers to save diligently towards that goal. Then, at the outset of the mortgage journey, young homebuyers would be required to devote the maximum amount they could afford from their disposable income towards repayments, as assessed by the lending institution”…

“The journey to home ownership and financial security across the life course clearly relied on a certain social compact: that wage growth would consistently outstrip inflation and keep pace with increases in home prices during a person’s working life”…

“The collapse in wage growth over the decade from 2012 to 2022 has hit young Australians particularly hard”…

Per Capita then argues that the suppression of wages after 2012, when Millennials and Gen Z Australians were in the first decade or so of their working lives, “not only robbed the average younger person of their first home deposit, but reduced their borrowing power”.

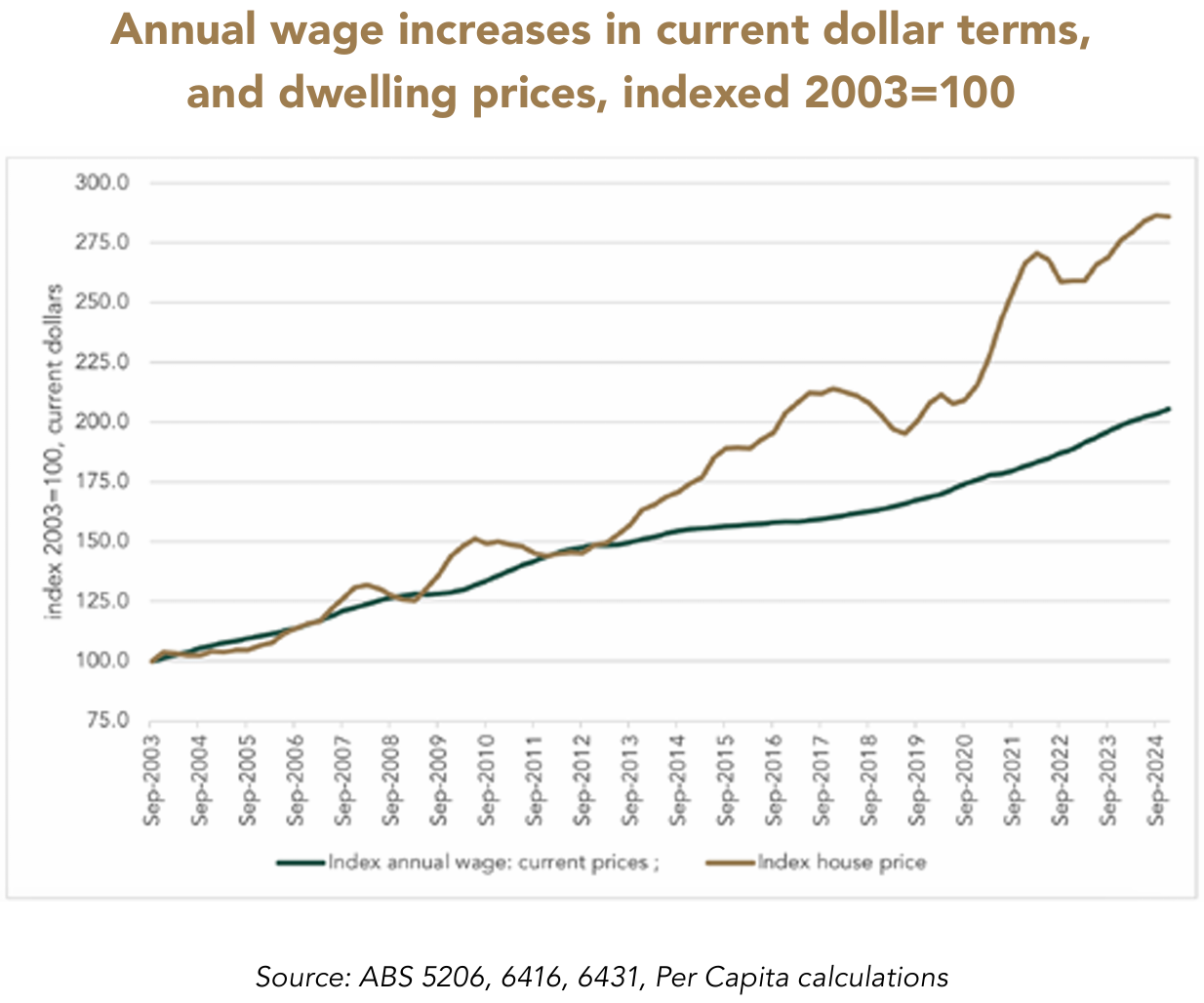

Over the same period, home prices soared:

“In the two decades between 2003 and 2024, while wages in current dollar terms doubled, house prices increased by nearly three times”, argued Per Capita.

“Almost all of the divergence of house prices from wages dates from 2012”.

Per Capita estimates that “workers were down an average of $4990 per year over the Lost Decade meaning, in nominal terms, $54,000 was removed from the pockets of working people and their households”.

As a result, they were unable to save a down payment for a home.

Per Capita then blames the Coalition’s Work Choices legislation for the anemic wage growth. It also claims that Labor has gotten real wages moving again.

“We find that a significant factor in the low wage growth of the Lost Decade was the introduction of WorkChoices legislation and its influence through the Fair Work Act”…

“It will take many years for the damage done in the Lost Decade of wage stagnation and soaring home prices to be addressed, but the fact that real wages are once again growing ahead of inflation, and starting to move into line with house prices, is an outcome young Australians cannot afford to risk”.

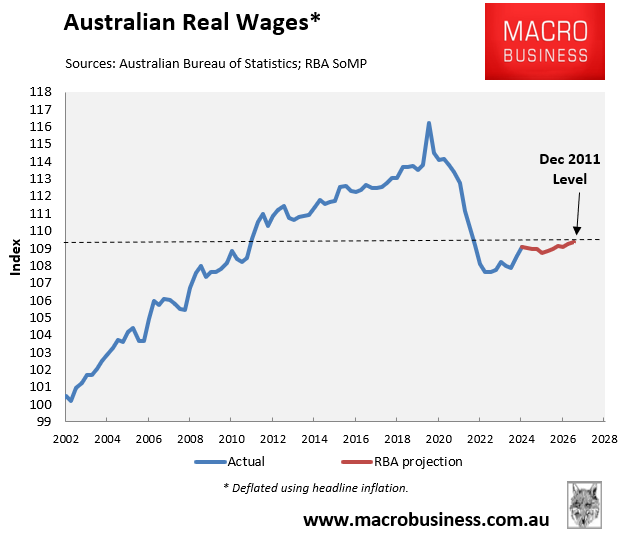

Of course, the RBA’s wage growth projections contradict Per Capita’s claim:

As usual, Per Capita refused to mention the pernicious impacts of running a high immigration policy.

Excessive levels of immigration are terrible for first-home buyers because:

- It drives up rents, making it much harder to save a deposit.

- It puts upward pressure on prices, increasing the deposit requirement and the amount that must be borrowed.

- It puts downward pressure on the wages of first home buyers, who must compete directly against migrants in the labour market.

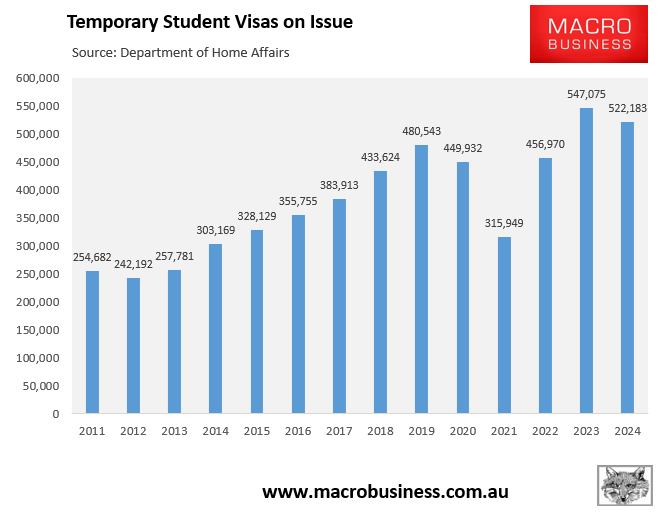

It is no coincidence that the number of student visas on issue has more than doubled since 2012:

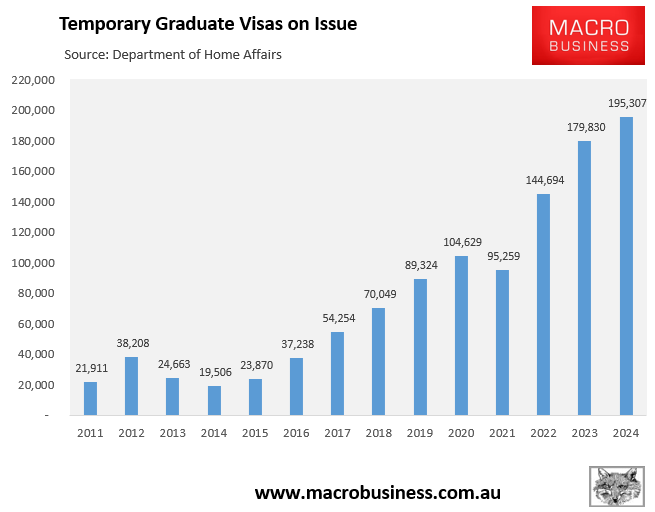

Or that the number of graduate visas on issue has exploded.

Who does Per Capita think these people compete with in the labour market? Younger Australians or older Australians?